Quarterly Estimated Taxes for Solo Shopify Founders

Last updated: 2026-06-30 · Estimated-tax thresholds, safe-harbor percentages, and due dates are set by the IRS and can change. Confirm current figures against IRS guidance or a qualified US tax professional before scheduling any payment.

A solo Shopify store does not withhold tax from its own profit. Every dollar of net profit lands in your account untaxed, and the IRS expects to be paid as that income is earned — not in one lump at filing time. For a founder whose store clears a few thousand dollars a month, that gap is where the January surprise and the underpayment penalty come from.

This guide covers the operating decision behind quarterly estimated taxes: whether you actually need to pay them, how much to set aside, and the four dates the payments are due. It is built around a single safe-harbor rule that, once you have one prior-year tax return, makes the whole thing penalty-proof and largely automatic.

The thresholds and dates here are 2026 planning figures drawn from IRS sources; the exact amount you owe depends on your filing status, other income, deductions, and state rules, so confirm the numbers against current IRS guidance or a CPA before acting.

This guide is part of Solo Shopify Taxes: The Complete 2026 Operating Guide — Forvendo’s hub covering income tax, sales tax, the 1099-K, and contractors.

Quick answer

- You generally need to pay quarterly estimated tax if you expect to owe $1,000 or more in federal tax for the year after subtracting withholding and credits (IRS, Estimated Taxes). Sole proprietors, single-member LLC owners, partners, and S-corp shareholders fall under this rule.

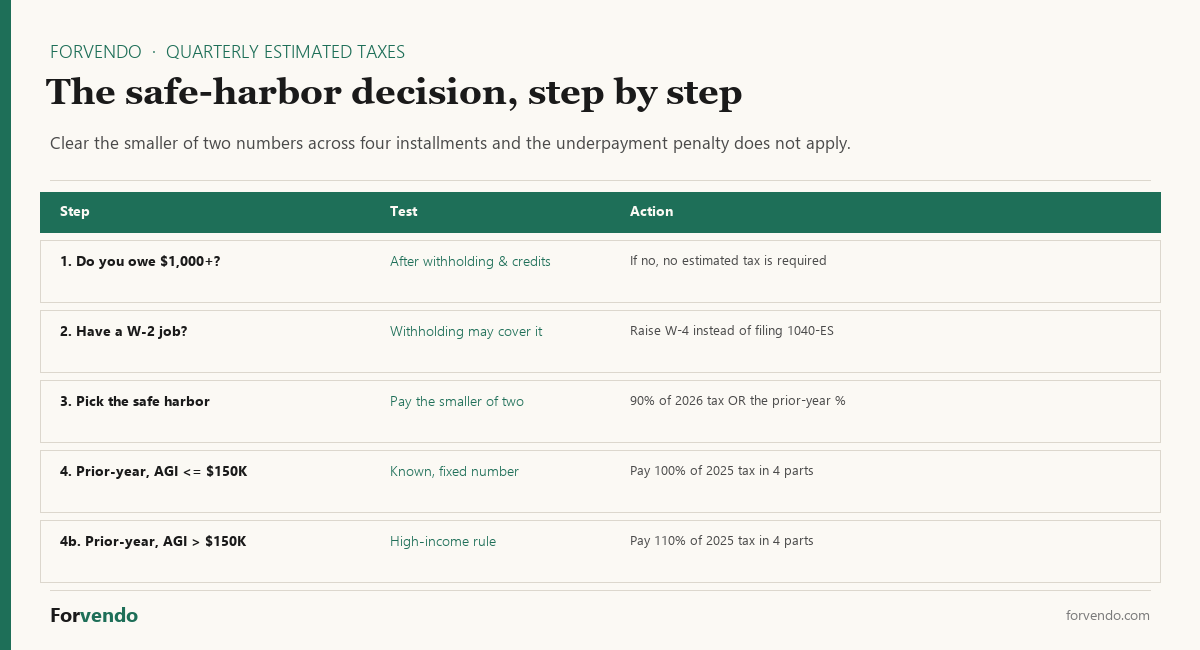

- The safe harbor makes it penalty-proof. You can avoid the underpayment penalty by paying the smaller of 90% of your 2026 tax or 100% of the tax shown on your 2025 return (2026 Form 1040-ES). If your 2025 adjusted gross income was over $150,000 ($75,000 if married filing separately), the prior-year figure rises to 110%.

- Payments use Form 1040-ES and are due in four installments. For the 2026 tax year (calendar-year filers): April 15, 2026 · June 15, 2026 · September 15, 2026 · January 15, 2027.

- A W-2 day job can absorb the store’s tax. If you also have employment income, raising your W-4 withholding is often simpler than filing 1040-ES — the IRS treats withholding as paid evenly across the year regardless of when it happens.

- A set-aside percentage keeps the cash ready. Moving a fixed share of every payout (a common planning range is 25–30% of net profit) into a separate account means the quarterly payment is already funded when the date arrives.

For the payment-side reporting that feeds your tax return, see 1099-K Reconciliation for Solo Shopify Operators. For sales tax — a separate obligation from income tax — see Multi-State Sales Tax for Solo Shopify Stores. If you pay contractors, W-9 and TIN Reconciliation covers the other side of the 1099 system.

Table of Contents

Who this is for

This article is written for the same operator as the rest of Forvendo’s tax coverage.

- You sell on Shopify in the United States, typically on the Basic plan.

- Monthly revenue sits between $5,000 and $50,000, and the store turns a net profit.

- You operate as a sole proprietor or single-member LLC (income flows to your personal 1040).

- You may also have a W-2 job, or the store may be your only income.

- You want to know whether quarterly payments apply to you, how much to set aside, and when to pay.

If your business is taxed as an S corporation paying you a salary, part of this changes — payroll withholding covers some of the obligation, and the planning runs differently. If your only concern is sales tax collected from customers, that is a separate system covered in the multi-state guide above; this article is about income tax on your profit.

Why estimated tax exists

The US income tax is pay-as-you-go. For an employee, that happens automatically: an employer withholds tax from each paycheck and sends it to the IRS. A solo Shopify founder has no employer doing that, so the system asks you to make the payments yourself, four times a year.

The mechanism that enforces it is the underpayment penalty. If you owe more than the $1,000 threshold at filing time and did not pay enough during the year, the IRS charges interest on the shortfall, calculated period by period on Form 2210. The penalty is not catastrophic — it is an interest charge, not a fine — but it is avoidable, and avoiding it is almost entirely a matter of paying on a schedule rather than paying the right amount to the dollar.

That distinction is the key to making this simple. You do not need to predict your exact tax to stay penalty-free. You need to clear a safe-harbor number, and the safe harbor can be set from a figure you already have: last year’s tax.

Do you need to pay? The $1,000 rule

The first decision is whether quarterly estimated taxes apply to you at all. Two situations let many side-store operators skip 1040-ES entirely.

Forvendo decision rule

Pay quarterly estimated tax if you expect to owe $1,000 or more in federal tax for the year after withholding and credits. Below that, the IRS does not require estimated payments.

If you also have a W-2 job, check whether raising your W-4 withholding can cover the store’s tax instead. Withholding is treated as paid evenly across the year, so a single W-4 change in, say, August can still satisfy the full-year requirement — something a late estimated payment cannot do.

Do not file 1040-ES yet if a W-2 job already covers it. Many founders run the store alongside full-time employment. If your employer’s withholding already exceeds your total expected tax (store profit included), you may owe less than $1,000 at filing and need no estimated payments. Raising your W-4 withholding to cover the store’s profit is often simpler than quarterly filings, because it stays automatic and the timing penalty does not apply to withholding.

Pay quarterly if the store is your main income, or if withholding falls short. A founder with no W-2 job, or whose day-job withholding does not cover the store’s profit, will generally clear the $1,000 threshold once the store is profitable and should plan on quarterly payments.

The safe harbor: how to be penalty-proof

Once you know you need to pay, the safe harbor decides how much. This is the rule that removes the guesswork. The IRS lets you avoid the underpayment penalty by paying the smaller of two numbers across your four installments.

The prior-year method is the one that makes this manageable for a solo operator. Your 2025 tax is a fixed, known number sitting on your filed return. Pay that amount (or 110% of it if your 2025 AGI was over $150,000) in four equal installments across 2026, and you are inside the safe harbor regardless of how the store performs this year. If the store grows and you end up owing more, the extra is simply due at filing — with no penalty, because you met the safe harbor.

The current-year method (90% of this year’s tax) can mean smaller payments if you expect the store to earn less than last year, but it requires estimating a number you do not know yet. For most founders, the prior-year safe harbor is the simpler, lower-risk default. The current-year method is worth using only when you have a clear reason to expect lower income.

One detail worth knowing: the IRS generally expects the installments to be roughly even across the four periods. Paying the full year’s safe-harbor amount in equal quarters satisfies that. If your income is highly seasonal, the annualized income installment method on Form 2210 can match payments to when income is actually earned, but for a steady store the even-installment approach is simpler.

How much to set aside

The safe harbor tells you the floor for penalty protection. A set-aside percentage tells you how to keep that cash available without thinking about it each month.

Your tax on store profit has two layers as a sole proprietor: self-employment tax (Social Security and Medicare on net self-employment earnings) and federal income tax at your marginal rate. State income tax may add a third, depending on where you live. Because those layers stack, the share of profit that needs to go to tax is higher than many founders expect — which is why a flat set-aside percentage, moved the moment a payout lands, prevents the cash from being spent before the quarterly date.

Set-aside worksheet

- Pick a set-aside rate. A common planning range for a profitable solo store is 25–30% of net profit; confirm your own rate with a CPA, since it depends on your bracket, state, and the self-employment tax interaction.

- Each time the store pays out, move that percentage of the period’s net profit into a separate tax savings account.

- On each due date, pay the safe-harbor installment from that account.

- At year-end, true up: if the set-aside account holds more than the tax owed, the surplus is yours; if less, top up before filing.

The set-aside percentage is a cash-flow tool, not a tax calculation. The safe harbor decides whether you owe a penalty; the set-aside decides whether the money is there to pay it.

The two tools work together. The safe harbor sets the minimum you pay each quarter to stay penalty-free; the set-aside builds the reserve those payments come from. A founder who does both rarely has a January surprise, because the cash was separated all year and the quarterly payments already cleared the safe-harbor bar.

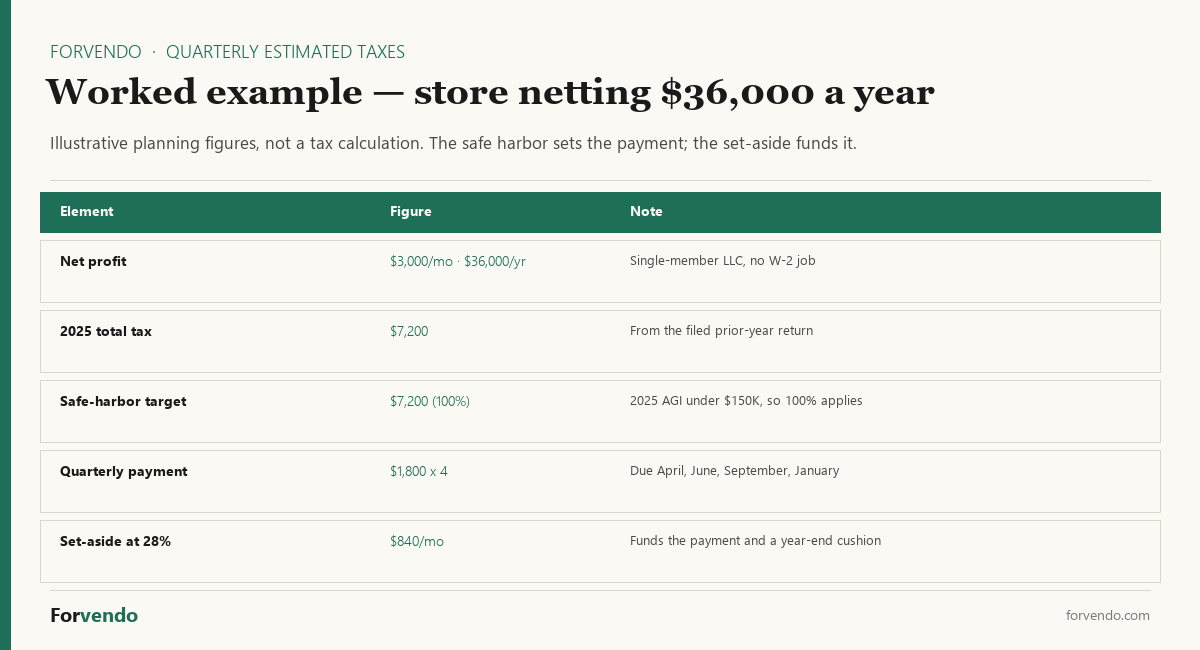

A worked example

These figures are illustrative planning numbers, not a tax calculation for any real return. They show the mechanics, not a rate you should copy.

Consider a single-member LLC store that nets $3,000 a month in profit — $36,000 for the year — and has no W-2 job. The operator filed a 2025 return showing $7,200 in total tax and had a 2025 AGI under $150,000.

Safe-harbor target (prior-year method). Paying 100% of the 2025 tax keeps the operator penalty-free: $7,200 for the year, split into four installments of $1,800 due in April, June, September, and January. That number is locked regardless of how 2026 turns out.

Set-aside (forward-looking). At a 28% set-aside rate on $3,000 of monthly profit, the operator moves $840 a month — $2,520 a quarter — into a tax account. That comfortably funds the $1,800 quarterly safe-harbor payment and builds a cushion for any true-up at filing.

Year-end true-up. If 2026 profit holds near 2025, the actual tax lands close to the $7,200 already paid through the safe harbor, and the leftover set-aside is the operator’s. If the store grows and the real 2026 tax is higher, the difference is due at filing in April 2027 — with no penalty, because the prior-year safe harbor was met every quarter.

The point of the example is the order of operations: the safe harbor sets the payment, the set-aside funds it, and the true-up reconciles. None of the three requires predicting the year accurately.

The four 2026 due dates

For a calendar-year filer, the 2026 estimated-tax installments are due on these dates (2026 Form 1040-ES). Each of the four 2026 dates falls on a weekday, so no weekend or holiday shift applies this year.

The quarters are not even three-month blocks — the first covers three months, the second two, the third three, and the fourth four. That is a quirk of the system, not a typo. The fourth installment also has an escape hatch: you can skip the January 15, 2027 payment if you file your full 2026 return and pay the entire balance by February 1, 2027 (IRS, When to Pay Estimated Tax).

Payments can be made through IRS Direct Pay, the Electronic Federal Tax Payment System (EFTPS), or by mailing the 1040-ES voucher. Direct Pay from a bank account is free and the cleanest paper trail for a solo operator.

Common mistakes

- Spending the profit, then scrambling at the due date. Without a set-aside account, the quarterly payment competes with inventory and operating cash. Separate the tax money the moment a payout lands.

- Treating sales tax money as profit. Sales tax you collect from customers is not your income — it is held on behalf of the state. Estimated income tax is calculated on profit, after that pass-through is removed.

- Assuming a W-2 refund means you are covered. A day-job refund can disappear once store profit is added. Check the combined picture before deciding to skip estimated payments.

- Forgetting state estimated tax. Many states with an income tax run their own quarterly estimated system with separate vouchers and, sometimes, different dates. Confirm your state’s rules alongside the federal ones.

- Trying to calculate the exact tax each quarter. The safe harbor exists so you do not have to. Paying the prior-year safe-harbor amount in even installments is simpler and removes the penalty risk.

- Missing the even-installment expectation. Paying the whole year’s amount in Q4 can still trigger a penalty for the earlier quarters. Spread the safe-harbor amount across all four dates.

What this article does not cover

This guide is scoped to federal quarterly estimated income tax for a solo Shopify operator taxed as a sole proprietor or single-member LLC. It does not cover state estimated-tax mechanics beyond noting that they exist, S-corporation payroll and reasonable-compensation rules, the detailed calculation of self-employment tax, the annualized income installment method in depth, or penalty abatement after a missed payment. It also does not address sales tax, which is a separate obligation covered in the multi-state sales tax guide. Any of those situations benefits from a qualified US tax professional.

Related Forvendo guides

Estimated taxes are one block in the store’s financial operating system. The 1099-K Reconciliation guide explains how the income figure that drives your tax actually arrives from Shopify Payments, and why the 1099-K is not your revenue. Multi-State Sales Tax for Solo Shopify Stores covers the separate sales-tax obligation that founders often confuse with income tax. If you pay contractors, W-9 and TIN Reconciliation handles the 1099-NEC side of the same annual cycle. The Solo Shopify Weekly Operating Checklist is where the quarterly tax review fits into a recurring cadence.

Download the Estimated Tax Planner

The companion sheet turns the safe harbor and set-aside into a working tool: a prior-year safe-harbor calculator (100% / 110%), a set-aside percentage worksheet, and a 2026 quarterly due-date tracker.

Download the Estimated Tax Planner 2026 · XLSX

Estimated Tax Safe-Harbor Calculator

Planning estimate based on the prior-year safe harbor, not tax advice. Confirm with a CPA.

Forvendo newsletter

Operating notes, once a week

One email a week for US-based solo Shopify operators at $5,000–$50,000 MRR: a decision, a checklist, or a teardown. No fluff, unsubscribe anytime.

Join the newsletter →Frequently asked questions

Do I have to pay quarterly estimated taxes if my Shopify store is a side project?

Only if you expect to owe $1,000 or more in federal tax after withholding and credits. If your W-2 job withholds enough to cover both your salary and the store’s profit, you may owe less than that and need no estimated payments. Raising your W-4 withholding is often the simpler way to cover side-store profit, because withholding is treated as paid evenly through the year.

How do I avoid the underpayment penalty without knowing my exact income?

Use the prior-year safe harbor. Pay 100% of the tax shown on your prior-year return (110% if your prior-year AGI was over $150,000), split into four equal installments. That keeps you penalty-free even if the store earns more this year; the extra is simply due at filing, without penalty.

What are the 2026 estimated tax due dates?

For calendar-year filers: April 15, 2026; June 15, 2026; September 15, 2026; and January 15, 2027. You can skip the January 15 payment if you file your full 2026 return and pay the balance by February 1, 2027.

How much of my Shopify profit should I set aside for taxes?

A common planning range is 25–30% of net profit for a profitable solo store, because self-employment tax and federal income tax stack on top of each other, and state tax may add more. Your actual rate depends on your bracket, filing status, and state — confirm it with a CPA. The set-aside is a cash-flow habit; the safe harbor is what determines the penalty.

Is estimated income tax the same as the sales tax I collect from customers?

No. Sales tax is collected from customers and remitted to the state on their behalf — it is not your income. Estimated income tax is paid on your store’s profit. They are separate systems with separate filings, and treating collected sales tax as profit is a common and costly mistake.

Can I just pay everything once a year instead of quarterly?

If you owe $1,000 or more and pay only at filing, you will generally owe an underpayment penalty for the quarters you skipped, even if you pay in full in April. The penalty is an interest charge calculated period by period, so spreading the safe-harbor amount across all four due dates is what avoids it.

Forvendo Editorial note. Forvendo publishes educational operating resources for solo ecommerce operators. Articles may cover tax, sales tax, 1099-K reporting, software pricing, platform policies, and other operating topics that change over time.

This content is for general research and operational planning. It is not legal, tax, accounting, financial, or professional advice. Readers should verify details with official sources or qualified professionals before acting on them. Platform rules, tax thresholds, software pricing, and affiliate program terms can change without notice.

Forvendo articles may be drafted with AI assistance and are reviewed by the operator before publication according to our Editorial Policy, which covers sourcing, AI use, update cadence, and corrections. See also About, Disclosure, and Privacy Policy.