W-9 Form and TIN Reconciliation for Solo Shopify Operators

Last updated: 2026-05-22 · IRS 1099-NEC reporting thresholds change in 2026 under the One Big Beautiful Bill Act (OBBBA). Confirm current thresholds against IRS guidance or a qualified US tax professional before deciding whether to issue a 1099-NEC for any given vendor.

A solo Shopify operator who pays a virtual assistant, freelance designer, photographer, or any other US-based contractor should have a W-9 form on file before the first payment goes out, and a TIN reconciliation done before the end of January.

The rules around when to collect a W-9 form, when a 1099-NEC is required, and what happens if a Tax Identification Number is missing or incorrect changed meaningfully under OBBBA in 2026. This W-9 and TIN reconciliation guide walks through the operating workflow — when to request a W-9 form, how to verify the TIN before it becomes a problem, how to respond to an IRS B Notice if one arrives, and the new $600 vs $2,000 threshold timeline that affects every solo operator with contractors.

The thresholds, dates, and dollar figures here are planning assumptions; the exact treatment depends on payment type, contractor status, and the tax year, so confirm against current IRS guidance.

This guide is part of Solo Shopify Taxes: The Complete 2026 Operating Guide — Forvendo’s hub covering income tax, sales tax, the 1099-K, and contractors.

Quick answer

- Request a W-9 before the first payment, not after. IRS Form W-9 (current revision 03/2024) is the IRS-blessed way to collect a contractor’s TIN, legal name, and federal tax classification. Without it, you may need to apply 24% backup withholding.

- The 1099-NEC reporting threshold is in transition. For tax year 2025 (payments made through December 31, 2025; filed January 2026), the threshold is $600. For tax year 2026 (payments made on or after January 1, 2026; filed January 2027), the threshold rises to $2,000 under OBBBA Section 70433, with annual inflation adjustment starting 2027.

- TIN Matching is a free pre-filing IRS service that validates TIN-name combinations before you submit 1099-NEC forms. Using it after each W-9 is received prevents most B Notice problems before they start.

- If the IRS sends a CP2100 or CP2100A notice, you have 15 business days to send a B Notice to the affected payee. If the payee does not respond within 30 days, backup withholding (24%) can begin on future payments.

- E-filing is required for 10 or more information returns (aggregated across all 1099 form types), effective for returns filed January 1, 2024 and later.

For the broader payment-side reconciliation, see 1099-K Reconciliation for Solo Shopify Operators. For multi-state sales tax context, see Multi-State Sales Tax for Solo Shopify Stores: A 2026 Operating Guide.

Table of Contents

- Who this is for

- Why W-9 timing matters

- The 1099-NEC threshold timeline ($600 vs $2,000)

- The W-9 and TIN reconciliation workflow

- TIN Matching — the free IRS pre-filing service

- What happens if a B Notice arrives

- State-level 1099 filing — the $2,000 federal threshold complication

- Common mistakes

- What this article does not cover

- Frequently Asked Questions

Who this is for

This article is built for the same reader as the rest of Forvendo’s tax coverage.

- You sell on Shopify in the United States, typically on the Basic plan.

- Monthly revenue sits between $5,000 and $50,000.

- You pay between 1 and 10 US-based contractors in a calendar year — virtual assistants, freelance designers, photographers, copywriters, accountants, or specialists you hire on a project basis.

- You operate the store alone or with a part-time helper.

- You want to know when to collect a W-9, when a 1099-NEC is required, and what changes in 2026.

If you have employees on payroll (W-2), the rules differ — W-2 employment uses different reporting. If you pay only non-US contractors, Form W-8BEN or W-8BEN-E applies instead of W-9.

Why W-9 form timing matters

The single most common solo-operator mistake on the 1099 side is collecting the W-9 late — either after the first payment, or only at the end of the year when 1099-NEC filing approaches. Two structural reasons this is the wrong order.

Backup withholding obligations. When a payer makes a reportable payment to a contractor whose correct TIN is not on file, IRS guidance states “the payer is required to withhold at the current rate of 24 percent” (Backup Withholding Program, IRS.gov). For a solo operator paying a virtual assistant $1,500 per month, that is $360 the operator would otherwise have to deduct, remit to the IRS, and reconcile on quarterly payroll deposit Form 945. Collecting the W-9 before the first payment avoids the entire backup withholding mechanism.

Reconciliation under time pressure. Trying to collect W-9s from five contractors in mid-January, after the calendar year has closed, often takes longer than the operator has before the January 31 filing deadline. Contractors disappear, change addresses, or simply do not prioritize sending tax forms back. The 1099-NEC filing deadline generally does not move when a W-9 arrives late.

A W-9 collected at contractor onboarding takes about three minutes. A W-9 collected in panic in January takes about three hours of follow-up — when it can be collected at all.

Forvendo decision rule

Collect every W-9 before the first contractor payment, not at year-end. A W-9 collected at onboarding takes three minutes; one collected in January takes three hours of follow-up — when it can be collected at all.

If a contractor refuses to provide a W-9, treat that refusal as a hard stop on payment. Backup withholding at 24% is a worse outcome for both parties than a five-minute conversation at onboarding.

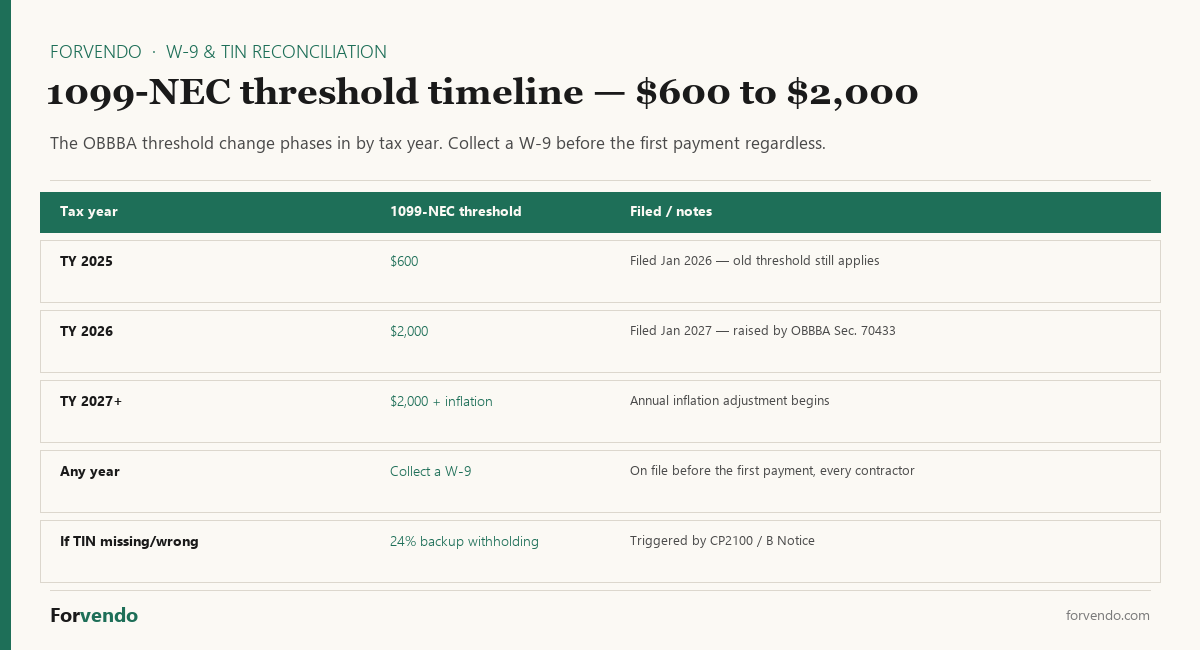

The 1099-NEC threshold timeline ($600 vs $2,000)

OBBBA Section 70433 raised the 1099-NEC reporting threshold but the effective date matters. The transition runs across two tax years.

Two implications for a solo Shopify operator reading this in 2026:

For 1099-NEC filed January 2026 (covering TY 2025 payments): the $600 threshold still applies. If you paid a contractor $750 in calendar year 2025, you should still issue a 1099-NEC. The OBBBA $2,000 threshold does not apply retroactively to TY 2025.

Free download

The Solo Shopify Weekly Operating Checklist

A one-page PDF plus a copyable Google Sheet — the weekly cadence these guides build on. Free; bring your own store data.

Get the free checklist →For 1099-NEC filed January 2027 (covering TY 2026 payments): the $2,000 threshold applies. A contractor paid between $600 and $2,000 in 2026 no longer triggers a federal 1099-NEC requirement.

State-level requirements are separate. New Jersey, for example, retains a $1,000 1099 filing threshold under state law, which now sits below the federal $2,000. A New Jersey contractor paid $1,500 in 2026 may not require a federal 1099-NEC but may require a state 1099 filing. Confirm against each state’s information-return rules.

The W-9 form and TIN reconciliation workflow

The pattern below applies to most solo Shopify stores paying US contractors. The same workflow scales from one contractor to ten.

Step 1 — At contractor onboarding, request the W-9 form. Before any payment, send the contractor the current IRS W-9 form (rev. 03/2024). Most solo operators store the blank W-9 form in a “Contractor Onboarding” folder and email it as part of the first project agreement. The contractor completes name, business name (if applicable), federal tax classification, address, and TIN, then signs.

Step 2 — Verify the W-9 looks complete. Common gaps to check before filing it away:

– Name field matches the TIN type (SSN → individual name; EIN → business name)

– Federal tax classification box is checked (sole proprietor, LLC, S-corp, C-corp, partnership)

– TIN is filled (either SSN or EIN, not both at once)

– Signature and date present

Step 3 — Run TIN Matching before the first payment. The IRS TIN Matching program is a free pre-filing service through IRS e-Services. It returns whether the TIN-name combination matches IRS records. Running this immediately surfaces typos and mismatches while the contractor is still in onboarding mode and easy to reach. Details in the next section.

Step 4 — Track payments by contractor across the year. A simple spreadsheet with one row per contractor, columns for each payment, and a running YTD total is sufficient for most solo operators. The companion W-9 / TIN Reconciliation Tracker automates this with a 1099-NEC trigger flag per row.

Step 5 — In January, file 1099-NEC for contractors above threshold. For TY 2025 filings (January 2026): contractors paid $600+ during 2025. For TY 2026 filings (January 2027 onward): contractors paid $2,000+ during 2026. Filing deadline: January 31 to both the IRS and the recipient.

Step 6 — E-file if 10 or more aggregate information returns. Under T.D. 9972, e-filing is required for returns filed January 1, 2024 and later when the payer files 10 or more information returns in aggregate (across 1099-NEC, 1099-MISC, 1099-K, W-2, etc.). Most solo operators with 5-10 contractors will cross the 10-return threshold once W-2s and other forms are counted.

TIN Matching — the free IRS pre-filing service

The IRS TIN Matching Program, accessible through IRS e-Services, “validates TIN and name combinations prior to submission of the information return” (IRS.gov). Interactive matching (up to 25 records per session) and bulk matching (up to 100,000 records, with 24-hour response) are both available. The service is free.

To enroll: register through IRS e-Services, complete the Payer Account File application, and wait for IRS approval (typically several days).

For a solo Shopify operator with 1-10 contractors, interactive TIN matching is sufficient. The recommended cadence is:

- After each new W-9 is received — run TIN matching immediately. If a mismatch is returned, contact the contractor while the project memory is fresh, not in January.

- Annually in early December — re-run TIN matching for all active contractors. Names sometimes change (marriage, business restructuring), and verifying before the January 31 filing deadline gives time to correct.

The match response is binary: TIN and name match IRS records, or they do not. A mismatch is not the same as a confirmed wrong TIN — sometimes the contractor’s IRS record uses a different name spelling, a hyphen, or a maiden name. The mismatch is a signal to follow up with the contractor, not an immediate trigger for backup withholding.

What happens if a B Notice arrives

A B Notice is the second-stage event in the backup withholding chain. The sequence:

1. IRS sends a CP2100 or CP2100A notice to the payer. This typically arrives in late summer or fall, listing payees whose TIN-name combinations did not match IRS records on the previously filed information return. CP2100 is the larger version (250+ payees, sent on CD); CP2100A is for fewer payees (under 50).

2. The payer has 15 business days to send a B Notice to the affected payee. The 15-day clock runs from the date on the IRS notice, not the date received. A first B Notice (1st-B) is required if the payee has not been listed on a CP2100/CP2100A in the past three years. The 1st-B requests a fresh Form W-9 from the payee.

3. The payee has 30 days to respond. If the payee returns a completed W-9 with the corrected information, the matter ends. If the payee does not respond within 30 days, the payer is required to begin backup withholding (24%) on future reportable payments.

4. If the same payee appears again on a CP2100/CP2100A within three years, a second B Notice (2nd-B) is required — and the requirements escalate. The 2nd-B does not request a new W-9; it requires the payee to obtain TIN validation directly from the Social Security Administration (SSA) for individuals (a copy of the Social Security card) or from the IRS for businesses (Letter 147C for an EIN). The payer still has 15 business days to send the 2nd-B.

5. If the payee does not respond to the 2nd-B within 30 days, backup withholding continues until proper TIN validation is received.

The operating lesson: TIN Matching at W-9 receipt is the cheapest insurance against B Notices. The 15-business-day window is short, and managing B Notice correspondence for multiple contractors during a busy operating season is a clear path to missed deadlines.

State-level 1099 filing — the $2,000 federal threshold complication

The federal threshold rising to $2,000 in TY 2026 creates a new compliance asymmetry that did not exist before. Several states maintain 1099 filing thresholds at or below the prior federal $600 level. When the federal threshold rises above the state threshold, contractors paid in those states may require a state 1099 filing without a corresponding federal 1099-NEC.

Examples to confirm against state-specific rules (this table reflects 2026-05-22 published thresholds and may shift):

| State | State 1099 threshold | Federal 1099-NEC threshold (TY 2026+) |

|---|---|---|

| Most states | Follows federal | $2,000 |

| New Jersey | $1,000 | $2,000 — state filing may apply between $1,000 and $2,000 |

The point is structural rather than state-specific: when the federal threshold moves above state thresholds, payers paying contractors in those states now have a federal-vs-state gap to manage. A solo operator paying contractors across multiple states should confirm whether each state’s threshold matches or sits below the new federal $2,000.

Five-record readiness check before issuing a 1099-NEC

- W-9 on file with a valid TIN

- TIN matched against IRS records via the free TIN Matching service

- Year-to-date payment log totals reaching the applicable threshold ($600 for TY 2025, $2,000 for TY 2026+)

- Contractor classification confirmed (1099 contractor vs W-2 employee — not casual)

- State-specific 1099 threshold check completed for the contractor’s state

If any record is missing, do not issue the 1099-NEC until it is corrected. Incorrect filings trigger CP2100 / B Notice cascades that take months to unwind.

Common mistakes

The patterns below cause most avoidable W-9 and 1099-NEC problems.

- Collecting W-9s after the first payment — by the time the contractor has been paid, the leverage to obtain a clean W-9 has dropped meaningfully. Collect at onboarding.

- Assuming the $2,000 threshold applies to TY 2025 payments — it does not. TY 2025 (filed January 2026) is still $600. The $2,000 applies to TY 2026 payments (filed January 2027).

- Ignoring TIN Matching — most B Notice problems are preventable through TIN Matching at W-9 receipt. The service is free.

- Missing the 15-business-day B Notice window — once a CP2100/CP2100A arrives, the clock is short. Calendar the deadline immediately.

- Not aggregating across information return types for the e-file threshold — the 10-return e-file rule aggregates 1099-NEC, 1099-MISC, 1099-K, W-2, and others. Five 1099-NECs alone do not require e-filing, but five 1099-NECs plus six W-2s do.

- Filing 1099-NEC without state-level review — federal compliance does not equal state compliance when state thresholds differ from federal. Particularly relevant from TY 2026 onward as the gap widens.

- Not preserving W-9 records — IRS guidance generally suggests retaining W-9s for at least four years after the last filing using the TIN. Cloud-based contractor folders solve this without ongoing effort.

What this article does not cover

This article is scoped to W-9 collection and 1099-NEC reconciliation for a solo Shopify operator paying US contractors. It does not cover:

- W-2 employment payroll, withholding, or quarterly Form 941 filings

- Non-US contractor payments (W-8BEN, W-8BEN-E, withholding rules)

- 1099-MISC payments for rent, royalties, prize income, or attorney fees

- 1099-K reconciliation for payments received through Shopify Payments (covered in 1099-K Reconciliation for Solo Shopify Operators)

- State-by-state filing requirements beyond illustrative examples

- IRS audit response procedures

- Penalty abatement requests after late filing

Any of those scenarios benefits from a qualified US tax professional.

Forvendo newsletter

Operating notes, once a week

One email a week for US-based solo Shopify operators at $5,000–$50,000 MRR: a decision, a checklist, or a teardown. No fluff, unsubscribe anytime.

Join the newsletter →Frequently Asked Questions

Does the new $2,000 1099-NEC threshold mean I do not need to file anything for contractors paid less than $2,000 in 2026?

For federal purposes, payments of less than $2,000 to a single contractor during tax year 2026 (made on or after January 1, 2026) do not generally trigger a federal 1099-NEC requirement. State requirements may still apply. The new federal threshold does not affect TY 2025 payments, which remain subject to the $600 threshold.

Do I need a W-9 if I am paying a contractor less than the 1099 threshold?

You do not legally have to issue a 1099-NEC below the federal threshold, but you should still collect a W-9 from any US contractor before payment. Without a W-9 (and the correct TIN), backup withholding rules can apply regardless of payment amount, and a W-9 collected at onboarding is cheap insurance against any future audit or threshold ambiguity.

What if a contractor refuses to provide a W-9?

IRS guidance requires that the payer apply 24% backup withholding on payments to a contractor who has not provided a correct TIN. Practically, a contractor refusing to provide a W-9 is a major risk signal for the payer — most legitimate US contractors provide one without issue.

How long do I have to file 1099-NEC after the calendar year ends?

January 31 of the following year, to both the IRS and the recipient. For TY 2025, the deadline is January 31, 2026. For TY 2026, the deadline is January 31, 2027.

Is paying through PayPal or Venmo subject to 1099-NEC reporting?

Payments through third-party settlement organizations (PayPal, Venmo for business, etc.) are generally reported on Form 1099-K by the platform, not on Form 1099-NEC by you. Direct payments via check, ACH, or wire transfer to a contractor are reportable by you on 1099-NEC if above threshold. Mixing payment methods within a single contractor relationship can complicate the reconciliation — confirm the reporting source for each contractor before filing.

Forvendo Editorial note. Forvendo publishes educational operating resources for solo ecommerce operators. Articles may cover tax, sales tax, 1099-K reporting, software pricing, platform policies, and other operating topics that change over time.

This content is for general research and operational planning. It is not legal, tax, accounting, financial, or professional advice. Readers should verify details with official sources or qualified professionals before acting on them. Platform rules, tax thresholds, software pricing, and affiliate program terms can change without notice.

Forvendo articles may be drafted with AI assistance and are reviewed by the operator before publication according to our Editorial Policy, which covers sourcing, AI use, update cadence, and corrections. See also About, Disclosure, and Privacy Policy.