Sales Tax Deregistration Workflow for Solo Shopify Stores

Last updated: 2026-05-22 · Sales tax registration rules vary by state and change between tax years. Confirm details directly with the relevant state Department of Revenue or a qualified US sales tax professional before closing any permit.

If you registered for sales tax in a state because of a temporary spike in revenue, a one-time transaction count event, or general caution, and your store has since settled below that state’s economic nexus thresholds, you may be a candidate for deregistration.

Deregistering when it is appropriate is not a tax avoidance step — it is operating hygiene. Each open permit creates a filing obligation, and unfiled returns generate notices, penalties, and account flags that take longer to resolve than they took to create.

This article walks through the practical workflow a solo Shopify operator can use to evaluate, prepare, and execute a sales tax permit closure in 2026, with four state walk-throughs covering California, Texas, New York, and Washington. The figures and timelines here are planning assumptions for a solo operator in the $5,000–$50,000 MRR band, not universal benchmarks; each state’s process and timing differ.

This guide is part of Solo Shopify Taxes: The Complete 2026 Operating Guide — Forvendo’s hub covering income tax, sales tax, the 1099-K, and contractors.

Quick answer

- Deregistration is a four-step workflow: confirm nexus has ended, file a marked-final return, submit the state’s closure form, and update Shopify so collection stops.

- You typically do not deregister the day you drop below the threshold. Most states use a 12-month lookback, and a single quarter below threshold is not enough.

- The final return is the most important step. Closing a permit without filing a final return is the single most common cause of post-closure notices.

- Each state runs its own closure process. This article walks through CA, TX, NY, and WA as worked examples; the same four-step pattern applies in other states with different form names.

- Records should be kept for at least four years in most states. California explicitly requires four years; New York and Texas use longer windows in some scenarios.

The article that follows assumes you have already read Multi-State Sales Tax for Solo Shopify Stores: A 2026 Operating Guide, which covers the threshold landscape and when deregistration becomes a candidate move in the first place.

Table of Contents

- Who this is for

- Why deregistration matters for a solo operator

- Before you start: confirm nexus has actually ended

- The four-step deregistration workflow

- State walk-through: California (CDTFA)

- State walk-through: Texas (Comptroller)

- State walk-through: New York (DTF)

- State walk-through: Washington (DOR)

- Updating Shopify after deregistration

- Deregistration checklist

- Common mistakes

- What this article does not cover

- Frequently Asked Questions

Who this is for

This article is built for the same reader as the rest of Forvendo’s tax coverage.

- You sell on Shopify into multiple US states.

- Monthly revenue sits roughly between $5,000 and $50,000.

- You currently hold a sales tax permit in at least one state where your trailing 12-month sales sit clearly below that state’s economic nexus thresholds.

- You operate the store alone or with a part-time helper. You handle your own filings, possibly with a tax software tool or a CPA on a per-task basis.

- You want a clear closure procedure rather than a year-long ambiguity about whether a permit should remain open.

If you have an active CPA managing your sales tax across many states, this article can still serve as a checklist before your closure meeting. If you are pre-revenue or registered in only one state, deregistration is rarely the right move yet.

Why sales tax deregistration matters for a solo operator

An open sales tax permit is not a passive line in your tax dashboard. It is an active filing obligation that produces returns, even when no tax is collected. Most states require a zero return if you remain registered and made no taxable sales during the period. A zero return takes only a few minutes to file, but missing one triggers a delinquency notice. Two or three of those across multiple states can absorb an entire weekend.

For a solo operator running on roughly 5 to 10 hours per week, the per-state friction of remaining registered where no obligation exists looks like this:

- Filing time: 15 to 30 minutes per period per state, even at zero revenue

- Mental load: tracking which periods are due across two to ten states

- Risk: delinquency notices and small penalties that compound while you are busy with the store

Deregistering where the underlying obligation has ended converts that ongoing tax to a one-time closure cost. That is the operating reason to do it.

Before you start: confirm nexus has actually ended

Deregistering too early is a worse outcome than waiting. If you drop below threshold for one quarter and bounce back the next, you may be required to re-register, file a back return for the gap, and pay penalties for the period you were out of compliance. Most economic nexus thresholds use a trailing 12-month lookback, so a single low quarter is not enough.

A conservative rule of operating practice:

- Pull a 12-month rolling sales report for the state.

- Confirm the most recent four quarters are all clearly below the threshold (not within 20 percent of it).

- Confirm you no longer have any physical nexus in the state — no inventory, no employees, no contractor, no event presence.

- Confirm you do not anticipate exceeding the threshold within the next two quarters based on your current run rate.

If all four checks pass for a given state, deregistration is a candidate move. If any single check is uncertain, hold the permit and revisit next quarter.

The free Sales Tax Nexus Tracker automates these four checks against 47 states + DC. Paste your trailing 12-month state-by-state revenue and transaction counts, and the sheet auto-flags each state as OVER REVENUE, OVER TX, WATCH, or OK. Use it before opening any deregistration form to confirm a state has actually fallen below threshold and is not within 20 percent of bouncing back.

The four-step sales tax deregistration workflow

The same four-step pattern applies across most states, with state-specific form names and portals. Each step has a clear “done” condition.

Free download

The Solo Shopify Weekly Operating Checklist

A one-page PDF plus a copyable Google Sheet — the weekly cadence these guides build on. Free; bring your own store data.

Get the free checklist →This pattern handles the majority of solo-operator scenarios. State-specific quirks change only the labels and the portal, not the four steps.

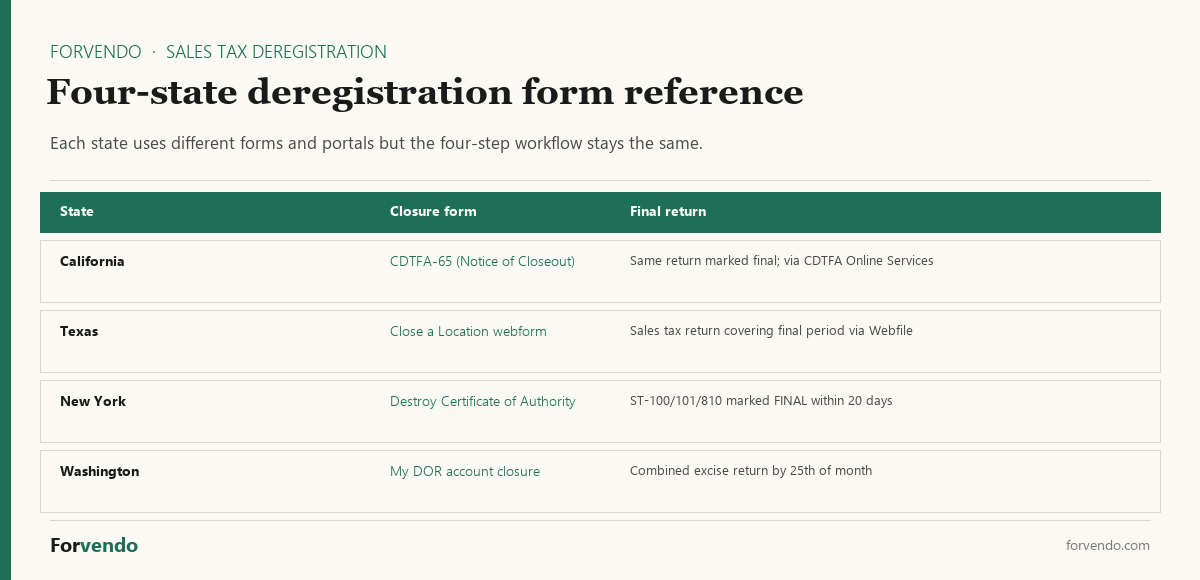

State walk-through: California (CDTFA)

California uses the California Department of Tax and Fee Administration (CDTFA) for seller’s permit management.

Final return. Before closing, file your final California sales and use tax return. If you are an electronic filer, the return form is the same one you normally file (CDTFA-401-A2 or similar, depending on your filing status); when filing, indicate that this is the final return. Pay all outstanding tax, fees, and penalties.

Closure form. California uses CDTFA-65, Notice of Closeout (current revision REV. 34, dated 1-20). According to CDTFA Publication 74, you can notify CDTFA either through Online Services or by completing CDTFA-65. Online closure runs through the CDTFA Online Services portal; the paper CDTFA-65 form is the alternative. Paper forms are mailed to California Department of Tax and Fee Administration, Customer Service Center, PO Box 942879, Sacramento, CA 94279-0090.

Records. Publication 74 states: “you must keep records for four years after closure of your account.” Most operators keep them longer, but four years is the floor.

Things to watch. California explicitly warns that failing to notify CDTFA when a business is sold can create successor liability — the buyer may inherit unpaid amounts. For a pure closure rather than a sale, this is less relevant, but it is the underlying reason why CDTFA expects a formal closure notice rather than simply ceasing filings.

State walk-through: Texas (Comptroller)

Texas closures go through the Texas Comptroller of Public Accounts.

Final return. The Comptroller’s “Close a Location” webform states explicitly: “Sales taxpayers closing a place of business are responsible for filing a sales tax return covering the final filing period.” File this through Webfile, the Comptroller’s online filing portal.

Closure form. Texas uses an online “Close a Location” webform (also listed on the Sales and Use Tax overview page as “Close One or More Locations”) at comptroller.texas.gov/web-forms/manage-account/close-location/. To submit, you need your 11-digit Texas taxpayer number, the relevant outlet (location) number, the last day of business at that location, and a security identifier from a recent return (total sales, total amount paid, or total revenue from previous year). You can close all outlets under a taxpayer number or only specific outlets.

Records. Texas does not publish a uniform retention period on this webform; the operating rule is to keep records for at least four years, and longer if there is any open audit or assessment.

Things to watch. Texas treats locations as distinct outlets even when a single taxpayer number covers them all. Online sellers without a physical Texas presence still need the outlet/location identifier the Comptroller assigned when the permit was issued.

State walk-through: New York (DTF)

New York closures go through the New York Department of Taxation and Finance (DTF).

Final return. DTF Tax Bulletin TB-ST-265, Filing a Final Sales Tax Return, specifies the form by filing status:

- Annual filers: Form ST-101

- Quarterly filers: Form ST-100

- Part-quarterly (monthly) filers: Form ST-810 for the quarter, plus Form ST-809 for the relevant monthly periods

The bulletin directs filers to write “FINAL RETURN” across the top of the form and check the box that marks the return as a final return. Web filers select the equivalent checkbox in the online return and enter their last day of doing business. According to the bulletin, the final return is due within 20 days after business operations cease.

Certificate of Authority. New York uses a Certificate of Authority rather than a separate close-out form. DTF Tax Bulletin TB-ST-25, Amending or Surrendering a Certificate of Authority, directs operators to surrender or destroy the Certificate of Authority when the business stops. The bulletin also clarifies that the certificate does not need to be physically returned to the Tax Department; the operator’s copy should be destroyed. After the final return processes, DTF inactivates the sales tax account.

Records. New York generally requires sales tax records to be kept for at least three years from the due date of the return, with longer windows for some categories. Confirm the current retention period with a New York tax professional if your case involves audit history.

State walk-through: Washington (DOR)

Washington closures go through the Washington Department of Revenue (DOR).

Final return. Washington uses the combined excise tax return. DOR’s closure guidance directs operators to file an excise tax return and pay outstanding taxes by the 25th of the month following the last day of business. The same return form normally used is filed for the final period, with the closure noted.

Closure form. The fastest path is My DOR, the online portal at secure.dor.wa.gov/home/. DOR states that My DOR is “the fastest way to close your account.” A paper alternative exists in the form of the Business Information Change Form (form number 700160).

Records. Washington generally requires business records to be kept for at least five years. Confirm specific periods with DOR or a Washington tax professional, especially if your business included use tax exposure.

Four states at a glance

The same four-step workflow runs through four different state interfaces. The matrix below summarises the closure form, the final return form, and the online portal for each.

The labels change; the four steps do not.

Updating Shopify after deregistration

Once the state has accepted your closure, the last step is to stop Shopify from continuing to calculate sales tax for that state.

In Shopify Admin, tax registrations live under Settings > Taxes and duties. According to Shopify’s official help documentation, the procedure to remove a US state registration is:

- Open your Shopify Admin

- Go to Settings > Taxes and duties

- Open the relevant country or region (United States)

- Find the registration you want to remove

- Click the … menu next to it

- Select Stop collecting

Shopify’s documentation notes specifically for the United States: “You can update the sales tax ID or advanced options, or choose Stop collecting for a state.” Confirm by placing a test draft order in checkout with a shipping address in the deregistered state and verifying that the order summary no longer adds that state’s sales tax.

Do not click Stop collecting in Shopify before the state has accepted your closure. If the state needs additional information and you have already stopped collection in your store, you may have a temporary gap where tax should still be collected pending the state’s confirmation.

This article points to Shopify’s official taxes and duties documentation for current button labels and any 2026 interface changes; the menu path above reflects the long-standing Shopify Admin structure but is worth confirming against your specific admin.

Sales tax deregistration checklist

A printable version of this checklist will be published as part of the planned Sales Tax Deregistration Kit. For now, the inline checklist below covers the operating moves.

- [ ] Pull a 12-month rolling sales report for the state

- [ ] Confirm the four most recent quarters are all clearly below threshold

- [ ] Confirm no physical nexus (inventory, employees, contractors, events)

- [ ] Save the dated sales report PDF in your records folder

- [ ] File the final sales tax return for the state, marked as final

- [ ] Pay all outstanding tax, fees, and penalties shown on the final return

- [ ] Submit the state’s closure form or online closure

- [ ] Save the closure confirmation number or screenshot

- [ ] Click Stop collecting on the state’s tax registration in Shopify Admin (Settings > Taxes and duties)

- [ ] Place a test draft order shipping to the state and confirm no tax is added

- [ ] Update your tracker sheet to mark the state as deregistered with the closure date

- [ ] Calendar a six-month review to confirm no notices have been received

A realistic closure timeline

Once you decide to deregister, the workflow runs over a few weeks rather than a single afternoon. State portals take time to acknowledge final returns and closure forms, and rushing the Shopify update can create a collection gap. A typical operator timeline looks like this.

The exact days vary by state. Online closures through state portals are often acknowledged within one to four weeks; paper closures can take longer. Plan for a one-month window rather than a one-week sprint.

Common mistakes

A handful of patterns generate most of the post-closure problems for solo operators.

- Closing the permit without filing a final return. The state’s system sees a registration in good standing, then sees a closure with an unfiled period. This is the single most common cause of post-closure notices.

- Deregistering after a single low quarter. Economic nexus uses a trailing 12-month window. A bounce-back quarter can put you back over threshold and force a re-registration with a gap.

- Removing the Shopify registration before the state confirms closure. If the state needs additional information, your store may temporarily under-collect.

- Discarding records too early. Four years is the floor in most states; closure does not end audit risk.

- Confusing permit closure with entity dissolution. Closing a sales tax permit does not close the underlying LLC or other business entity. Those are separate filings with the Secretary of State, typically.

Forvendo decision rule

Deregister only after two consecutive quarters of trailing-12-month revenue sitting clearly below 80% of the state’s threshold. A single low quarter is not enough — economic nexus uses a 12-month lookback, and re-registering after a bounce-back quarter typically costs more than holding the permit one extra quarter.

File the final return before submitting the closure request, not after. State systems frequently flag “closure without final return” as the single most common post-closure notice trigger.

What this article does not cover

This article is scoped to the operating workflow for sales tax permit closure. It does not cover:

- Federal tax obligations (1099-K, income tax). See the article on 1099-K reconciliation for the federal side.

- Dissolution of an LLC, corporation, or other business entity.

- Multi-state voluntary disclosure agreements (VDAs) for periods of past unfiled returns.

- Bulk sale notifications when selling a business to another operator.

- Sales tax obligations created by marketplace facilitator arrangements rather than direct sales.

Any of those scenarios benefits from a qualified professional.

Forvendo newsletter

Operating notes, once a week

One email a week for US-based solo Shopify operators at $5,000–$50,000 MRR: a decision, a checklist, or a teardown. No fluff, unsubscribe anytime.

Join the newsletter →Frequently Asked Questions

How long does sales tax deregistration take?

Closure timing varies by state. Online closures through state portals are often acknowledged within one to four weeks, sometimes faster. Paper closures can take longer. The article does not estimate exact processing times because they shift with state staffing and time of year; confirm the current expected window with the state’s published guidance.

Do I need to file a return if I had no sales in the final period?

In most states, yes. A final return at zero is still a return, and marking it as final is the operating signal that distinguishes it from an ongoing zero return. Skipping the final return is the most common cause of post-closure delinquency notices.

Can I deregister in one state while staying registered in others?

Yes. Sales tax registrations are independent by state. Deregistration in one state has no automatic effect on your obligations in other states.

What happens if I deregister and then exceed the threshold again?

You may be required to re-register, file returns for any period after re-crossing the threshold, and potentially pay penalties for the gap. This is why most operators wait until they are clearly and stably below threshold before closing a permit.

Do I need a CPA to deregister?

For straightforward cases — a clean sales history, a single permit, no open audit — solo operators routinely complete deregistration without a CPA. For cases involving past unfiled returns, audit notices, business sales, or multi-state simultaneous closures, a CPA or sales tax specialist is a reasonable investment.

Forvendo Editorial note. Forvendo publishes educational operating resources for solo ecommerce operators. Articles may cover tax, sales tax, 1099-K reporting, software pricing, platform policies, and other operating topics that change over time.

This content is for general research and operational planning. It is not legal, tax, accounting, financial, or professional advice. Readers should verify details with official sources or qualified professionals before acting on them. Platform rules, tax thresholds, software pricing, and affiliate program terms can change without notice.

Forvendo articles may be drafted with AI assistance and are reviewed by the operator before publication according to our Editorial Policy, which covers sourcing, AI use, update cadence, and corrections. See also About, Disclosure, and Privacy Policy.