Multi-State Sales Tax for Solo Shopify Stores: A 2026 Operating Guide

Last updated: 2026-05-21 · Sales tax rules and 1099-K thresholds change between tax years and by state. Confirm details with the relevant state tax agency or a qualified US sales tax professional before acting on filings or registrations.

If you sell on Shopify into more than one US state, the rules for when you may need to register, when you may be able to deregister, and when filings are required can change every six to twelve months.

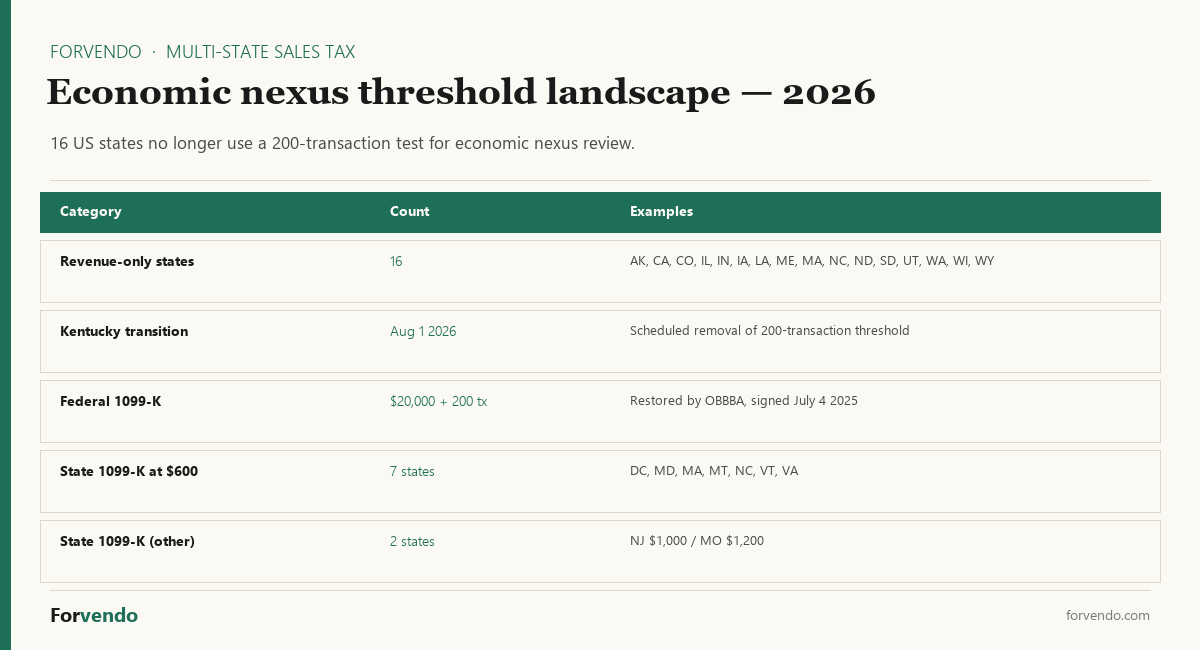

2025 and 2026 are unusually active years — 16 states now use revenue-only economic nexus thresholds or no longer use a 200-transaction test, the federal 1099-K threshold reverted to $20,000 and 200 transactions, and 7 states still enforce state-level 1099-K reporting at $600.

This article maps the current landscape for a solo Shopify operator in the $5,000–$50,000 MRR band and gives you a practical operating framework you can run in about thirty minutes a quarter. The dollar figures, thresholds, and time estimates here are planning assumptions for that band, not universal benchmarks; actual obligations depend on where inventory sits, sales volume by state, and each state’s current rules.

This guide is part of Solo Shopify Taxes: The Complete 2026 Operating Guide — Forvendo’s hub covering income tax, sales tax, the 1099-K, and contractors.

Quick answer

- 16 states are treated in this guide as revenue-only states for economic nexus review. Some have been revenue-only historically; others removed the 200-transaction test in 2025 or 2026. Solo Shopify stores that registered only because of transaction count, not revenue, may be able to deregister in those states.

- Kentucky is scheduled to remove the 200-transaction threshold on August 1, 2026 under Kentucky House Bill 757. Plan around the date.

- The federal 1099-K threshold reverted to $20,000 plus 200 transactions under the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025.

- 7 states still issue state-level 1099-K at $600 with no transaction minimum: DC, MD, MA, MT, NC, VT, VA. Two more enforce $1,000 (NJ) and $1,200 (MO).

- A solo operator can typically organize multi-state sales tax exposure in about one evening per quarter using a tracker sheet. The article that follows walks through the framework, with conservative language because state rules change.

Detailed multi-state sales tax registration, filing, and deregistration obligations should be confirmed with the relevant state tax agency or a qualified US sales tax professional before acting on them.

Table of Contents

- Who this is for

- The core problem: sales tax is state-by-state

- Key definitions

- Why solo Shopify operators get confused

- The 2026 threshold landscape

- A practical sales tax operating framework

- Multi-state risk checklist

- Example: A composite $18,000 MRR operator across five states

- Shopify-specific considerations

- When to use software vs when to ask a professional

- What this article does not cover

- Practical next steps

- Frequently Asked Questions

Who this is for

This article is built for a specific reader. If most of the following describes you, the framework should fit your store.

- You sell on Shopify, typically on the Basic plan or Shopify (not Plus).

- Monthly revenue sits roughly between $5,000 and $50,000.

- You ship into more than one US state. Two states is enough to make multi-state thinking relevant.

- You operate the store alone or with a part-time helper. You do not have an internal tax team.

- You use Shopify Tax or another tax-calculation tool, but you do not yet have a clear picture of where you should be registered, which states require filings, and which registrations may be candidates for deregistration in 2026.

- You spend roughly 5–10 hours a week on the store. You want a quarterly cadence, not a daily ritual.

If you are pre-revenue, sell exclusively through a single marketplace integration (where the marketplace facilitator handles tax), or run a multi-state operation with several employees and a CPA on retainer, the framework still has useful parts, but the calibration is different. Pre-revenue operators should focus on getting to first revenue. Multi-employee operations usually need a dedicated tax workflow built with their CPA.

This article does not provide individual legal or tax advice. Anything that affects your filings should be reviewed with a qualified professional licensed in the relevant state.

The core problem: sales tax is state-by-state

US sales tax is administered by states (and in some cases counties or cities), not by the federal government. There is no single national sales tax registration, no single national sales tax return, and no single national rate.

For a solo Shopify operator selling into multiple states, this creates a fundamental operating reality:

- Each state defines what creates a sales tax obligation in that state.

- Each state defines its own revenue threshold, transaction threshold, and effective date.

- Each state runs its own registration process.

- Each state runs its own filing calendar (monthly, quarterly, or annual).

- Each state runs its own deregistration process when an obligation ends.

Even after the 2018 South Dakota v. Wayfair Supreme Court decision created the modern framework for economic nexus, the implementation rules have stayed state-specific. A workflow that works for California will not directly translate to North Carolina or Texas. A federal 1099-K threshold that changes does not automatically change state 1099-K thresholds.

This is the problem the rest of this article tries to organize.

Key definitions

Solo operators often pick up the vocabulary in pieces from various sources. Here are the seven terms that show up in most sales tax conversations, defined in plain language for an operator audience. These definitions are educational starting points, not legal definitions. State law and case law can shape each one differently.

Physical nexus. A connection between a seller and a state that comes from a physical presence in that state. A home office, an employee, a contractor performing work in the state, inventory stored in a 3PL warehouse in the state, attending a trade show with sales activity in the state — each can create physical nexus, depending on the state’s specific rules.

Economic nexus. A connection between a seller and a state that comes from selling above a defined revenue or transaction threshold into that state, even without any physical presence. Most states use a revenue threshold (often $100,000) and used to also use a transaction threshold (often 200 transactions); the trend in 2025–2026 is toward revenue-only thresholds.

Marketplace facilitator. A platform such as Amazon, Etsy, or Walmart that facilitates sales between third-party sellers and buyers. Most states require the marketplace facilitator to collect and remit sales tax on behalf of the seller for sales made through the marketplace. Direct sales through your own Shopify store are generally not covered by the marketplace facilitator rules and remain the seller’s responsibility. Marketplace facilitator rules can reduce collection and remittance work for marketplace orders, but whether marketplace sales count toward a seller’s economic nexus threshold varies by state. Operators should check each state’s current guidance before excluding marketplace sales from a threshold review.

Registration. The administrative act of registering with a state’s tax agency (often called Department of Revenue or Department of Taxation) for a sales tax permit or seller’s permit. Registration is what allows a seller to legally collect sales tax from buyers and remit it to the state.

Collection. Adding the correct sales tax to the buyer’s invoice at checkout, based on the buyer’s location and the seller’s registration status, and holding that money in trust for the state until remittance.

Filing. Submitting the state’s required sales tax return (monthly, quarterly, or annual depending on the state and the seller’s volume) that reports gross sales, taxable sales, and tax collected.

Remittance. Paying the collected sales tax to the state by the filing deadline. A return without remittance is incomplete; remittance without a return is also incomplete.

For operators new to the vocabulary, the most useful mental separation is: registration is annual or one-time, collection is per-order, filing is recurring, remittance is per-filing. They are related but not the same activity.

Why solo Shopify operators get confused

Multi-state sales tax confuses solo operators for predictable, structural reasons. Naming them helps.

The first reason is that state rules change at different cadences from federal rules. The IRS sets the federal 1099-K threshold; individual states set their own state-level 1099-K thresholds. When the federal rule reverts under OBBBA but state thresholds stay at $600, an operator who tracks only the federal change still has an unmet state-level reporting trigger.

The second reason is that economic nexus thresholds are conjunctive in some states and disjunctive in others. A state with an “OR” rule treats either revenue or transaction count as a trigger; a state with an “AND” rule needs both. The 16 simplification states above moved to revenue-only thresholds, removing the transaction-count side entirely.

The third reason is that marketplace facilitator rules can hide a real obligation behind a perceived one. Sales through Amazon may not count toward your own state thresholds, but direct Shopify sales into the same state do. Operators who run both channels sometimes see their Amazon orders in dashboards and assume their Shopify orders are covered too.

The fourth reason is that Shopify Tax can calculate and collect once a state is set up, but it cannot register you or file your returns. The tooling and the obligation are not the same thing, and conflating them is a common confusion point.

The fifth reason is that state DOR pages and Shopify Help Center pages both update without notification. A workflow that was correct six months ago may need to be re-checked because a state changed its threshold, registration process, or filing cadence.

The framework below tries to absorb these confusions rather than ignore them.

The 2026 multi-state sales tax threshold landscape

This section is the reference map. Use it as a starting point, then confirm each state’s current threshold against the state’s own Department of Revenue page before acting on it. State rules can shift mid-year through new legislation.

Sales tax economic nexus — states with revenue-only thresholds

These 16 states now use a revenue-only economic nexus threshold (some historically, others after removing the 200-transaction test in 2025 or 2026). If your gross sales into the state are below the revenue threshold, you generally do not have economic nexus in that state, regardless of how many orders you shipped there.1

Free download

The Solo Shopify Weekly Operating Checklist

A one-page PDF plus a copyable Google Sheet — the weekly cadence these guides build on. Free; bring your own store data.

Get the free checklist →| State | Revenue threshold | Removed 200-tx test |

|---|---|---|

| Alaska | $100,000 (administered by local commission) | Effective Jan 1, 2025 |

| California | $500,000 | Historic (always revenue-only) |

| Colorado | $100,000 | Historic |

| Illinois | $100,000 | Effective Jan 1, 2026 |

| Indiana | $100,000 | Historic |

| Iowa | $100,000 | Historic |

| Louisiana | $100,000 | Historic |

| Maine | $100,000 | Historic |

| Massachusetts | $100,000 | Historic |

| North Carolina | $100,000 | 200-transaction test no longer used; confirm current effective date with NCDOR |

| North Dakota | $100,000 | Historic |

| South Dakota | $100,000 | Historic |

| Utah | $100,000 | Historic |

| Washington | $100,000 | Historic |

| Wisconsin | $100,000 | Historic |

| Wyoming | $100,000 | Historic |

Kentucky is scheduled to remove the 200-transaction threshold on August 1, 2026. If a Kentucky registration is based purely on transaction count, a deregistration may be possible after that date — confirmed with Kentucky’s Department of Revenue.

For North Carolina, confirm the current remote-seller threshold and effective date against current NCDOR guidance before acting.

This table is an operating reference, not a state-by-state legal determination. Thresholds, effective dates, and marketplace-sales treatment should be checked against each state’s current Department of Revenue guidance before registration, filing, or deregistration decisions.

Sales tax nexus — states that still enforce a transaction threshold

The remaining states keep the original “either revenue or transaction count” rule. A solo operator shipping a high volume of small-dollar items into one of these states can still trigger economic nexus on count alone. Confirm the current rule with the state’s Department of Revenue before relying on this article — state nexus rules can change with new legislation each session.

Federal vs state 1099-K reporting in 2026

Federal threshold (post-OBBBA): $20,000 in gross payments AND 200 transactions on a single platform in a calendar year. Shopify Payments issues a 1099-K when both conditions are met.2

State-level 1099-K thresholds that may apply below the federal floor:

| State | Threshold | Transaction minimum |

|---|---|---|

| District of Columbia | $600 | None |

| Maryland | $600 | None |

| Massachusetts | $600 | None |

| Montana | $600 | None |

| North Carolina | $600 | None |

| Vermont | $600 | None |

| Virginia | $600 | None |

| New Jersey | $1,000 | None |

| Missouri | $1,200 | None |

Practical effect: a solo seller whose state of residence falls in the $600 group can receive a state-issued 1099-K from Shopify Payments even when total annual volume is below the federal $20,000 threshold. Verify each state’s current 1099-K threshold with the state Department of Revenue before filing, because pages and rules can change between tax years.

Backup withholding — the silent risk

If a payment processor (Shopify Payments included) cannot match the seller’s Taxpayer Identification Number (TIN) to IRS records, and the seller’s transactions cross the reporting threshold, the processor may be required to apply 24% backup withholding to gross payouts until the TIN issue is resolved.3

For a solo operator running $25,000 in monthly volume, this means roughly $6,000 a month held back by the processor — usually for several weeks while the W-9 on file is corrected. The fix is administrative, not financial: confirm Shopify Payments has the correct legal entity name and EIN or SSN on file before any threshold is crossed.

A practical multi-state sales tax operating framework

Most of the confusion described above goes away once a solo operator runs the same review on the same cadence. The framework below has five steps. Each one is a question, not a conclusion. The answers depend on your specific store and should be confirmed against current state guidance.

These five questions form the basis of the quarterly review. The Forvendo Solo Shopify Weekly Operating Checklist builds the cadence around them.

Forvendo decision rule

Register in a state on the date the trailing-12-month threshold is crossed, not at the start of the next calendar quarter. In many states, interest and penalties can begin from the obligation date rather than the discovery date, so confirm the rule with the state’s DOR or a qualified professional.

If a state’s trailing-12-month revenue or transactions sit within 10% of the threshold for two consecutive months, treat that as a registration trigger — start the registration paperwork in the second month rather than waiting for a third.

Multi-state sales tax risk checklist

The quarterly review is short by design. Most of the items below take a few minutes each. The structure is intentionally compact so the entire review fits in about thirty minutes per quarter.

The free Sales Tax Nexus Tracker Sheet (linked at the end of this article) automates the first two rows and gives you a printable view of the rest.

Example: A composite $18,000 MRR operator across five states

This is a composite example, not a case study from one specific store.

“Sam” runs a niche apparel store on Shopify Basic, average order value $52, ships about 350 orders per month into TX, NY, CA, NC, and IL. Sam is currently registered in NY and CA (legacy registrations from 2023, when transaction count still triggered economic nexus in NY). Sam did not register in NC, TX, or IL, because revenue into each was well below $100,000.

Walking through the 2026 map:

| State | 2025–2026 status | Sam’s exposure | Action |

|---|---|---|---|

| Texas | Revenue threshold $500,000 | ~$30,000 / year | No action |

| New York | Revenue $500,000 + transaction test (legacy nexus) | ~$24,000 / year, ~470 orders | Deregister candidate — well below $500,000 |

| California | Revenue $500,000 (historic, no transaction test) | ~$36,000 / year | Deregister candidate — well below $500,000 |

| North Carolina | Revenue $100,000 (200-tx removed Jul 2025) | ~$14,000 / year, ~270 orders | Deregister candidate — under revenue, transaction test removed |

| Illinois | Revenue $100,000 (200-tx removed Jan 2026) | ~$11,000 / year, ~210 orders | Deregister candidate — under revenue, transaction test removed |

Sam’s total time for the deregistration filings — assuming each state takes about 45 minutes once Sam’s identification numbers and 2025 totals are ready — is roughly 3.5 hours. Net result: Sam ends up filing four fewer state returns every quarter, which removes roughly 16 returns a year from the calendar.

State-level 1099-K does not apply to Sam in this example, but if Sam had sold $5,000 into one of the states with a $600 threshold (DC, MD, MA, MT, NC, VT, VA), Sam might receive a state-issued 1099-K from Shopify Payments and would need to review the corresponding state filing obligations. Sam would not have known this without checking the state-level 1099-K map. Confirm the current threshold with each state’s Department of Revenue before filing.

The exact deregistration sequence, the final return process for each state, and the timing rules should be verified against each state’s current guidance. Filing too early can be reversed if a year-end push pulls revenue back over the line. The companion article Sales Tax Deregistration Workflow for Solo Shopify Stores walks through the four-step closure pattern with worked examples for California, Texas, New York, and Washington.

Shopify-specific considerations

Shopify provides tooling that helps with sales tax but does not replace the operator’s responsibility for registration, filing, and remittance.

Shopify Tax can calculate sales tax at checkout based on the buyer’s location and the seller’s registered states. To work correctly, Shopify Tax typically needs:

- Each state where you are registered marked as active in the tax settings

- The correct sales tax permit number or registration number entered for each state

- Product tax categories assigned for items that have unusual taxability (digital products, clothing in some states, food in some states)

- Shipping taxability configured for each state, because some states tax shipping and others do not

The Shopify Help Center on US sales tax setup walks through the current configuration screens.

Shopify Payments is separate from Shopify Tax. Shopify Payments handles the payment processing, the W-9 on file, and the issuance of 1099-K forms when reporting thresholds are crossed. Mismatches between the legal entity name and TIN on file in Shopify Payments can trigger backup withholding even when sales tax is correctly configured.

Marketplace integrations through Shopify apps (Amazon, Etsy, Walmart connectors) generally do not pull the marketplace’s tax remittance into Shopify’s view of sales tax. The marketplace handles its own tax collection and remittance for sales made through the marketplace; Shopify Tax handles only the direct Shopify sales. The split matters when calculating nexus exposure.

Tax software outside Shopify (TaxJar, Avalara, Anrok, and similar) can integrate with Shopify to handle multi-state filing, automated registration in new states, and remittance scheduling. These tools have a cost and a setup curve. For solo operators in the $5,000–$50,000 MRR band, full automation is often premature; a tracker sheet and quarterly review may be enough until the store crosses around $40,000 MRR.

When to use software vs when to ask a professional

The line between tooling and professional help is real and worth thinking about explicitly.

- Sales by state are clear and well below most state thresholds

- The store ships exclusively through Shopify Payments

- Product tax categories are simple (apparel, general merchandise, accessories)

- The operator is comfortable reading a state DOR portal and filing a return

- The marketplace footprint is small or zero

- Approaching or crossing economic nexus in several states at once

- A state DOR has sent a notice, audit letter, or registration suggestion

- Inventory held in 3PL warehouses in multiple states (physical nexus)

- Digital products sold into states with different digital-goods rules

- Previous tax year filings appear inconsistent across states

- A structure change (entity, ownership) is being considered

- Accounting and 1099-K records do not reconcile cleanly

A qualified US sales tax professional can help with:

- Reviewing the historic registration footprint and flagging cleanup candidates

- Preparing voluntary disclosure agreements where past nexus may have been crossed without registration

- Designing a state-by-state filing calendar with realistic cadence

- Reviewing 1099-K reconciliation for accuracy

- Responding to state DOR notices or audit letters

Sales tax expertise is a specialised area. A general bookkeeper or a generalist CPA may or may not have the specific multi-state sales tax background needed. The Streamlined Sales Tax Governing Board publishes resources on participating states and a list of Certified Service Providers that can help when a multi-state filing footprint becomes complex.

See the full 2026 economic-nexus threshold table for all 50 states — filterable, with a free nexus checker.

What this article does not cover

This article is intentionally scoped to multi-state sales tax operations for solo Shopify operators. It does not cover:

- Individual legal or tax advice for any specific store, structure, or situation

- State-by-state tax determination for products with unusual taxability

- Federal or state income tax (the article touches 1099-K reporting only as it intersects with sales tax operations)

- VAT, GST, or any non-US tax regime

- Accounting cleanup, books reconciliation, or historic correction projects

- Audit defense or response to state DOR audit letters

- Entity-specific tax strategy (LLC, S-corp, sole proprietorship trade-offs)

- Use tax, business and occupation tax, or gross receipts taxes that some states impose alongside sales tax

- International sellers shipping into the United States from outside

Operators who need help in any of the above categories should reach out to a qualified US sales tax professional, a CPA, an attorney, or an enrolled agent licensed in the relevant jurisdiction.

Quarterly review trigger

The whole multi-state review compresses into about one hour per quarter once the workflow is in place.

- Pull trailing-12-month state-by-state revenue and transaction count (~30 min)

- Run the free Sales Tax Nexus Tracker against the pull (~20 min)

- Update the operating spreadsheet with state registration status and filing calendar (~10 min)

- Schedule any deregistration or registration moves for the next 30 days

One quarter skipped is usually recoverable. Two quarters skipped tends to surface as a state notice that takes longer to resolve than the four quarterly reviews would have taken.

Practical next steps

What to do this week, in order:

- Download the free Sales Tax Nexus Tracker Sheet linked below and load your trailing 12-month Shopify sales by state.

- Identify the top five states by revenue and compare each against the current state economic nexus threshold. Flag any state above 70% of its threshold.

- Check each currently registered state against the 16-state simplification list. For registrations that depended on the 200-transaction test in a state that removed it, list the deregistration timing.

- Confirm Shopify Payments has the correct legal entity name and TIN on file, especially if a 1099-K reporting threshold may be crossed this year.

- Schedule the next quarterly review for the end of the current quarter. Set the meeting with yourself in your calendar. Same day, same time, every quarter.

- List the questions for a qualified professional if any of the items in the “When to ask a professional” section above match your situation.

The Sales Tax Nexus Tracker Sheet is a free Google Sheet that captures trailing 12-month sales by state, the current threshold (revenue and transaction) for each state, and flags any state where exposure has crossed the line in the last review period. It is designed for a solo operator working one evening a quarter.

Download the free Sales Tax Nexus Tracker Sheet and use it as the base version before building a larger compliance system.

For operators with active deregistrations to file across multiple states, the Sales Tax Deregistration Workflow article covers the four-step closure pattern. The Sales Tax Deregistration Kit — planned for release — adds the state-by-state final-return templates and a tracker that flags re-registration triggers if revenue grows back.

Sales Tax Nexus Checker

A planning check, not a nexus determination. Thresholds vary by state and change; confirm with the state.

Forvendo newsletter

Operating notes, once a week

One email a week for US-based solo Shopify operators at $5,000–$50,000 MRR: a decision, a checklist, or a teardown. No fluff, unsubscribe anytime.

Join the newsletter →Frequently Asked Questions

Do I need to register in every state where I make a sale?

No. Registration generally depends on whether a state’s specific physical or economic nexus rules apply to your situation. Many states only require registration after a defined revenue or transaction threshold is crossed. The exact rules vary by state and can change between tax years. Confirm with the state’s Department of Revenue or a qualified professional before registering.

Does Shopify collect sales tax for me automatically?

Shopify Tax can calculate and collect sales tax at checkout for states where you have configured the tax settings and registered with the state. Calculation and collection are separate from registration and filing. Shopify cannot register your business with a state or file a return on your behalf.

What is economic nexus?

Economic nexus is a connection between a seller and a state created by selling above a defined revenue or transaction threshold into that state, even without any physical presence. The thresholds vary by state and the trend in 2025–2026 is toward revenue-only thresholds.

What is a marketplace facilitator?

A marketplace facilitator is a platform such as Amazon, Etsy, or Walmart that processes sales between third-party sellers and buyers. Most states require the marketplace facilitator to collect and remit sales tax on sales made through the marketplace, which generally means those sales do not count toward the seller’s own nexus thresholds in those states.

What should I review monthly?

Sales by state, threshold proximity for the top five states, and any state DOR correspondence received during the month. A deeper review of registration status, deregistration candidates, and the W-9 on file fits better in a quarterly cadence.

When should a solo Shopify operator talk to a sales tax professional?

When the store is approaching multiple state thresholds at once, when a state DOR notice has arrived, when inventory is held in 3PL warehouses across several states, when a structural change is being considered, or when previous filings do not reconcile cleanly. A specialist in multi-state sales tax can review the situation more efficiently than a generalist.

Does the OBBBA $20,000 federal threshold apply retroactively to 2024?

The OBBBA, signed July 4, 2025, retroactively restored the $20,000-and-200-transaction federal threshold for payments made after December 31, 2021, repealing the lower $600 threshold. Because the IRS had been applying transition relief in the prior years, 2024 reporting was not at the $600 level. For reconciling a 1099-K you receive, see the 1099-K Reconciliation workflow. Confirm against the IRS Form 1099-K FAQs current at filing.

If a state removed the 200-transaction threshold, do I need to file a final return before deregistering?

Many state DOR portals may expect a final return covering the period through the deregistration effective date. The exact filing sequence varies by state and should be confirmed against the state’s deregistration instructions. The Sales Tax Deregistration Workflow article walks through the four-step pattern with state-specific examples.

Can Shopify automatically deregister me?

Shopify can stop collecting sales tax in a state once that state’s registration is set to “Stop collecting” in Settings > Taxes and duties, but the actual deregistration filing with the state revenue agency is your responsibility. A registration left open without the state’s requested final return may create compliance issues.

-

State revenue agency pages list each state’s current economic nexus threshold and effective date. North Carolina example accessed 2026-05-20: https://www.ncdor.gov/taxes-forms/sales-and-use-tax/remote-sales — the precise effective date for North Carolina’s 200-transaction removal should be confirmed against the governing NCDOR notice before relying on the effective date. ↩

-

IRS, “About Form 1099-K.” Accessed 2026-05-20: https://www.irs.gov/forms-pubs/about-form-1099-k ↩

-

IRS, “Backup withholding.” Accessed 2026-05-20: https://www.irs.gov/businesses/small-businesses-self-employed/backup-withholding ↩

Forvendo Editorial note. Forvendo publishes educational operating resources for solo ecommerce operators. Articles may cover tax, sales tax, 1099-K reporting, software pricing, platform policies, and other operating topics that change over time.

This content is for general research and operational planning. It is not legal, tax, accounting, financial, or professional advice. Readers should verify details with official sources or qualified professionals before acting on them. Platform rules, tax thresholds, software pricing, and affiliate program terms can change without notice.

Forvendo articles may be drafted with AI assistance and are reviewed by the operator before publication according to our Editorial Policy, which covers sourcing, AI use, update cadence, and corrections. See also About, Disclosure, and Privacy Policy.