1099-K Reconciliation for Solo Shopify Operators: A Practical Workflow

Last updated: 2026-05-21 · 1099-K reporting thresholds, payment processor formats, and IRS guidance change between tax years. Confirm details with current IRS guidance, your payment processor’s documentation, or a qualified US tax professional before relying on this article for filing decisions.

If you accept payments through Shopify Payments, the 1099-K you receive in January generally does not match your Shopify revenue dashboard, your bank deposits, your accounting software, or your taxable income for the same year. That gap is structural, not an error. This article explains why the numbers differ, gives you a practical reconciliation workflow for a solo Shopify operator at $5,000–$50,000 MRR, and helps you prepare cleaner questions for a CPA, bookkeeper, or tax preparer.

This guide is part of Solo Shopify Taxes: The Complete 2026 Operating Guide — Forvendo’s hub covering income tax, sales tax, the 1099-K, and contractors.

Quick answer

- Form 1099-K reports gross payments processed by a payment platform, not net revenue, and not taxable income. The number Shopify Payments reports to the IRS is generally larger than what reached your bank account.

- Five line items typically explain most of the mismatch: refunds, chargebacks, payment processing fees, shipping income, and sales tax collected.

- A 1099-K reconciliation worksheet usually takes 30–45 minutes per tax year if done once during January, and considerably longer if it has to be reconstructed during filing.

- The federal 1099-K threshold reverted to $20,000 + 200 transactions under Section 70432 of the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025. The restoration is retroactive to tax year 2022. However, 9 US jurisdictions still issue state-level 1099-K at thresholds between $600 and $1,200, so many solo operators receive a state-issued 1099-K even with no federal one.

- The 1099-K reconciliation pattern below is the same pattern most CPAs follow. Store-specific treatment should be reviewed with a qualified tax professional.

The Forvendo multi-state sales tax operating guide covers the registration and state-threshold side. This article focuses on the 1099-K reconciliation workflow after 1099-K forms and payment records exist.

Table of Contents

- Who this is for

- Why your 1099-K does not match your bank deposits

- Key definitions

- The practical reconciliation framework

- The 5-line-item reconciliation model

- Shopify Payments records to export

- Example: A composite $192K-revenue Shopify operator

- Common mismatch scenarios

- Monthly reconciliation checklist

- The state 1099-K trap

- When to ask a CPA, bookkeeper, or tax professional

- What this article does not cover

- Practical next steps

- Frequently Asked Questions

Who this is for

This article is built for a specific reader.

- You sell on Shopify, typically on the Basic plan or Shopify (not Plus).

- You accept card payments through Shopify Payments (and possibly other processors such as PayPal or Shop Pay Installments).

- Monthly revenue sits roughly between $5,000 and $50,000, with annual gross payments likely above the federal reporting threshold of $20,000 plus 200 transactions, or above a state-level threshold.

- You have already received, or expect to receive, a Form 1099-K from Shopify Payments or another processor.

- You are confused because the 1099-K gross amount does not equal your bank deposits, Shopify payout totals, accounting revenue, or taxable income.

- You want a practical reconciliation workflow that produces a clear hand-off document for a CPA or bookkeeper.

The framework is also useful for operators who have not yet received a 1099-K but are approaching a reporting threshold. Knowing the reconciliation pattern in advance avoids a January scramble.

If your store is pre-revenue, sells exclusively through a marketplace facilitator (where the marketplace handles 1099-K reporting), or runs full enterprise accounting with a dedicated tax team, the article still has useful parts, but the calibration is different.

This article does not provide individual tax advice. Store-specific reconciliation, accounting method choices, and filing decisions should be reviewed with a qualified US tax professional.

Why your 1099-K does not match your bank deposits

If you exported a Shopify “Total sales” report for tax year 2025 and lined it up against the 1099-K from Shopify Payments, the numbers will generally not match. Operators see this every January. The mismatch is expected.

A Form 1099-K is required by the IRS to report gross payments processed by a payment settlement entity — the amount of customer money that flowed through the payment processor before any deduction. That number generally includes:

- Payments that were later refunded

- Payments that were later charged back

- The portion that funded shipping

- The portion that funded sales tax collected for state authorities

- The portion later paid to the processor as fees

Net business revenue, by contrast, is what you report on Schedule C (sole proprietorship) or the corresponding line on Form 1120, 1120-S, or 1065 (depending on entity type). That number generally excludes the items above, or treats them as separate line items elsewhere on the return.

The result is that a Shopify Payments 1099-K showing roughly $238,000 in gross payments can reconcile cleanly to about $192,000 of net business revenue for the same operator in the same year, with nothing inappropriate happening. The IRS receives both figures (the 1099-K from Shopify Payments, the Schedule C from you) and computer-matches them. A gap on its own is not a problem. A gap that cannot be explained is. The reconciliation workflow below is what produces the explanation in a few pages instead of a few weeks.

Form 1099-K is generally a payment-reporting form. It usually needs to be reconciled against refunds, fees, chargebacks, payout timing, and bookkeeping records before it can be used in tax preparation. Confirm the current IRS treatment with About Form 1099-K on IRS.gov before filing.

Key definitions

Reconciliation conversations move faster when the vocabulary is shared. The nine terms below show up in most 1099-K discussions for a Shopify operator. These are educational starting points, not legal definitions; specific tax treatment varies by accounting method, entity type, and state.

Form 1099-K. An IRS information return that a payment settlement entity (such as Shopify Payments, PayPal, or Stripe) issues to a seller and to the IRS to report the gross amount of payment card and third-party network transactions processed for the seller in a calendar year. The federal threshold reverted to $20,000 plus 200 transactions under OBBBA Section 70432 — retroactively applied to tax year 2022 onward; state thresholds vary.

Gross payments. The total dollar value of card and third-party-network payments processed for the seller during the period, before any deductions. This is the figure reported in Box 1a of Form 1099-K.

Refunds. Money returned to the buyer by the seller after the original payment was processed. A refund generally appears as a separate transaction in the processor’s ledger; the original charge usually remains in the 1099-K gross figure.

Fees. Amounts the processor deducts before paying out to the seller — typically a percentage of the transaction (often around 2.9% for US cards on Shopify Payments) plus a fixed per-transaction amount. Confirm the current fee schedule on Shopify’s own documentation before relying on a specific rate.

Chargebacks. A dispute initiated by the buyer’s card-issuing bank that pulls the original payment back from the seller. A chargeback won by the buyer generally removes the funds from the seller’s account but does not remove the original transaction from the 1099-K gross figure.

Payouts. The batched transfers from the processor to the seller’s bank account. A payout is generally net of fees and refunds processed during the batch window. Shopify Payments groups individual transactions into payouts on a schedule that depends on the seller’s bank, country, and payout settings.

Deposits. The credits that appear in the seller’s bank account when a payout settles. The deposit amount usually equals the payout amount, but timing can differ by 1–3 business days, which matters at year-end when payouts cross calendar boundaries.

Taxable income. The income reported on the seller’s tax return after applicable deductions and adjustments. Taxable income is not the 1099-K gross figure; it is what remains after refunds, fees, cost of goods sold, expenses, and other deductions, and depends on the entity’s accounting method. Definitions and treatment should be confirmed with a CPA.

Bookkeeping records. The seller’s own ledger of sales, refunds, fees, sales tax collected, and other transactions, kept in QuickBooks, Xero, Wave, a spreadsheet, or another accounting system. Bookkeeping records are the seller’s source of truth for filing; the 1099-K is a third-party verification.

The most useful mental separation: the 1099-K is a single-platform gross-payment report; the bookkeeping records are the seller’s full ledger; the tax return is the net-income filing. Reconciliation is the act of showing how the three relate.

The practical 1099-K reconciliation framework

The framework has six stages, each tied to a specific record. Each stage is a question, not a conclusion. The answers depend on the seller’s processor mix, accounting method, and state.

Free download

The Solo Shopify Weekly Operating Checklist

A one-page PDF plus a copyable Google Sheet — the weekly cadence these guides build on. Free; bring your own store data.

Get the free checklist →Reconciliation walks across these six stages and matches the totals at each one against the surrounding records. The 5-line-item model below is the compact version of the same workflow.

Forvendo decision rule

Reconcile a Shopify Payments 1099-K within 30 days of receiving the form, not the day before the filing deadline. The cost of catching a mismatch in February is one Sunday afternoon. The cost of catching it in April is an amended return and possibly an IRS notice 12 to 18 months later.

If the gap between 1099-K Box 1a and reported gross revenue is greater than 5%, treat it as a hard stop on filing until the five reconciliation line items have been walked.

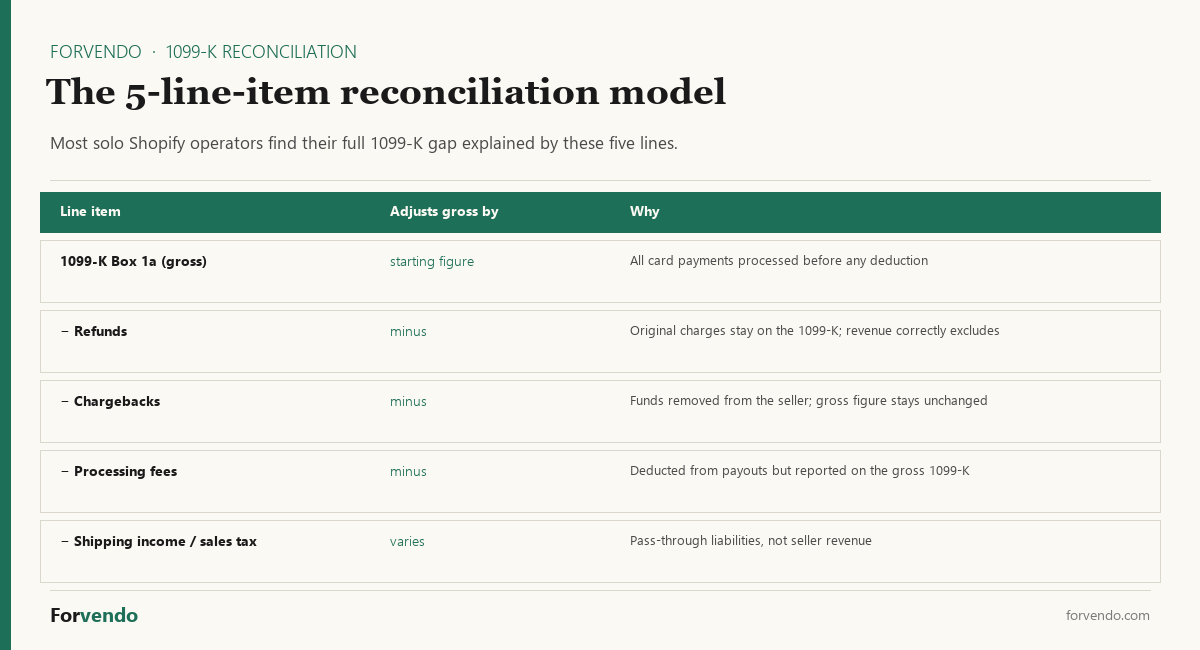

The 5-line-item 1099-K reconciliation model

Five line items typically explain most of the gap between a Shopify Payments 1099-K and the net business revenue reported on a tax return. The model is the same one most CPAs use when preparing or reviewing a return.

The numbers above are illustrative. Actual line items will differ by store, processor mix, and accounting method. The model does not replace tax or accounting advice — it is a reconciliation pattern that produces a clean hand-off document for a CPA or bookkeeper to review. Store-specific treatment should be confirmed with a qualified tax professional.

Shopify Payments records to export

The reconciliation needs six Shopify-side records and one 1099-K. All exports use the same calendar year date range that appears on the 1099-K.

| Source | Report or document | What it shows |

|---|---|---|

| Shopify admin → Settings → Payments → Shopify Payments → Documents | Form 1099-K | Box 1a gross amount for the tax year |

| Shopify admin → Analytics → Reports → Finances | Total sales | Total sales for the calendar year, used as the bookkeeping cross-check |

| Shopify admin → Analytics → Reports → Finances | Returns | Total refunds issued in the calendar year |

| Shopify admin → Analytics → Reports → Finances | Taxes | Sales tax collected (grouped separately by Shopify) |

| Shopify admin → Analytics → Reports → Finances | Shipping | Shipping revenue charged to customers |

| Shopify admin → Analytics → Reports → Finances | Payment provider fees | Total Shopify Payments fees for the year |

| Shopify admin → Analytics → Reports → Finances | Chargebacks | Chargebacks won by buyers (lost by the seller) |

Each report can be exported as CSV. The Shopify Help Center on Shopify reports covers the current export interface. The exact report names and structures can change as Shopify updates the admin interface.

If the store accepts payments through more than one processor (Shopify Payments plus PayPal, Stripe, Affirm, Shop Pay Installments, or others), each processor issues its own 1099-K when it crosses its own reporting threshold. The reconciliation needs to run separately for each processor and then be combined into a total ledger.

Example: A composite $192K-revenue Shopify operator

This is a composite example, not a case study from one specific store.

“Sam” runs the same niche apparel store referenced in the multi-state sales tax operating guide. Calendar 2025 1099-K from Shopify Payments arrives in mid-January 2026 showing $238,000 in Box 1a.

Sam’s reconciliation worksheet:

1099-K Box 1a (gross processed) $238,000

− refunds (179 orders @ ~$52.51 average) −9,400

− chargebacks (24 lost, total) −1,200

− shipping income (separated) −14,800

− sales tax collected (state liability) −11,200

− Shopify Payments fees (roughly 2.9% + $0.30) −9,400

─────────────────────────────────────────────────────

Net business revenue (cross-check baseline) $192,000

The Schedule C “Gross receipts or sales” line, after the reconciliation, shows $192,000. The IRS computer-matches the 1099-K Box 1a ($238,000) against the Schedule C ($192,000), sees the gap, and either accepts the gap as ordinary (the typical outcome when the gap is explainable by the five line items above) or sends a notice requesting explanation. If a notice arrives, Sam attaches the reconciliation worksheet and the supporting Shopify reports as the response.

Without the worksheet, the same notice can trigger several weeks of back-and-forth with a CPA, easily several hundred dollars in professional fees that did not need to happen. With the worksheet, the response is usually a three-page document and a short cover note.

Treatment of any specific line item — particularly processing fees, shipping income, and sales tax collected — depends on the seller’s accounting method and entity type, and should be confirmed with a CPA before filing.

Common mismatch scenarios

Even with the five line items above, a reconciliation can still produce a residual gap. The most common scenarios:

Third-party gateway under the same Shopify checkout. PayPal, Shop Pay Installments, and Affirm process payments outside Shopify Payments but still appear in the Shopify “Total sales” report. Each issues its own 1099-K (if its threshold is met). Subtracting one processor’s 1099-K from another processor’s totals can double-count or under-count revenue. The correct approach is generally to reconcile each processor separately, then add the results.

Mid-year processor change. Sellers who switched from one processor to another mid-year receive partial 1099-Ks from each, covering only the months each was active. Each partial 1099-K should be reconciled separately for the months it covers.

Year-end payout timing. A payout dated December 30 with a deposit on January 2 can be reflected in the 1099-K gross figure for the earlier year while the bank deposit lands in the next year. Cash-basis bookkeeping treats this differently from accrual-basis bookkeeping. The accounting method choice should be discussed with a CPA.

Gift card and store credit transactions. Some gift card flows process a card payment when the gift card is sold, with no immediate fulfillment, and a separate ledger entry when the gift card is later redeemed. Both may appear in different reports without obvious linkage. Confirm how Shopify’s current gift card reporting treats these flows.

Manual orders, third-party invoicing, or recurring billing apps. Orders created outside the standard Shopify checkout can be missed by some reports. Cross-checking the payouts report against bookkeeping income usually surfaces these.

Sales tax remittance mid-year. If a seller remits collected sales tax to a state monthly or quarterly, the cash leaves the bank account during the year but is not seller income at any point. Sales tax collected should already be excluded from net revenue per the model above; sales tax remitted is a separate liability flow.

Backup withholding. If the processor cannot match the seller’s Taxpayer Identification Number (TIN) to IRS records once a reporting threshold is crossed, the processor may be required to apply 24% backup withholding to gross payouts until the TIN issue is resolved.1 Withheld funds reduce deposits without changing the 1099-K Box 1a figure. The fix is administrative: confirm that the legal entity name and EIN or SSN on file in Shopify Payments match IRS records before any threshold is crossed.

If the reconciliation gap remains material after addressing the scenarios above, the gap is generally a signal to involve a CPA rather than to keep adjusting in isolation.

Quick reconciliation readiness test

Before opening the reconciliation spreadsheet, confirm these five inputs are pulled and saved:

- 1099-K Box 1a (gross) — exact dollar value from the form

- Shopify Payments annual payout total (Shopify admin → Finances → Payouts)

- Annual refund total (Shopify admin → Orders → filter by refund)

- Annual chargeback total (Shopify Payments → Disputes report)

- Annual processing fees (Shopify Payments → Reports)

If any input is missing, the reconciliation will not close cleanly. Stop and export first — usually faster than reverse-engineering totals later.

Monthly 1099-K reconciliation checklist

The annual reconciliation in January is easier when monthly records have been kept clean during the year. The checklist below is intentionally short so it fits inside a regular operating routine — for example, alongside the Solo Shopify Weekly Operating Checklist.

A small monthly habit prevents the entire December-into-January scramble that most solo operators experience the first time they receive a 1099-K.

The state 1099-K trap

The federal 1099-K threshold reverted to $20,000 plus 200 transactions under OBBBA, but several US jurisdictions continue to issue state-level 1099-Ks at lower thresholds. The multi-state sales tax operating guide covers the full state table; for reconciliation purposes, the key facts are:

- 7 states issue state-level 1099-K at $600 with no transaction minimum: DC, MD, MA, MT, NC, VT, VA.

- New Jersey issues at $1,000 with no transaction minimum.

- Missouri issues at $1,200 with no transaction minimum.

For a solo seller resident in any of those jurisdictions, a state-level 1099-K can arrive from Shopify Payments even when no federal 1099-K is issued. The reconciliation pattern is the same — the gross figure, less the five line items, gives the net for the state’s purposes. The complications:

- The state 1099-K may cover a different date range than the federal calendar year.

- The state may apply different sourcing rules (sales sourced to buyer location versus seller location).

- The state may not separate sales tax collected for that state from sales tax collected for other states.

For operators in a $600-threshold state, the reconciliation worksheet usually needs an additional column showing “in-state sales only” alongside total sales. State-specific 1099-K treatment should be confirmed with the state Department of Revenue or a CPA familiar with that state.

When to ask a CPA, bookkeeper, or tax professional

The reconciliation framework is designed to be runnable by a solo operator. The line between self-service reconciliation and professional involvement is worth thinking about explicitly.

- Single processor (Shopify Payments only)

- One state of residence and limited multi-state sales tax exposure

- Cash-basis or simple accrual bookkeeping is already in place

- Reports export cleanly and the five line items account for the gap

- No outstanding state DOR or IRS notices

- Multiple processors with separate 1099-K forms (Shopify Payments + PayPal + Affirm + others)

- Reconciliation gap remains material after the five line items are subtracted

- An IRS notice or state DOR notice has arrived

- Backup withholding has been applied to payouts

- A mid-year processor change, entity change, or accounting method change

- State-level 1099-K from a $600 jurisdiction with unfamiliar sourcing rules

- Prior tax year filings appear inconsistent with the reconciliation

A CPA, enrolled agent, or qualified tax preparer should be considered when the mismatch is material, when records are incomplete, or when prior filings may be affected. Sales-tax and 1099-K reconciliation expertise is a specific area — a generalist preparer may or may not have the multi-platform background needed for an ecommerce store. Asking about the preparer’s experience with Shopify Payments, Stripe, PayPal, and multi-state 1099-K reconciliation before engaging usually saves time on both sides.

What this article does not cover

This article is intentionally scoped to 1099-K reconciliation for a solo Shopify operator using Shopify Payments. It does not cover:

- Individual tax advice for any specific store, structure, or situation

- Choice of accounting method (cash vs accrual) — this should be discussed with a CPA

- Choice of entity type (sole proprietor, LLC, S-corp, C-corp, partnership) and the tax-return form that follows

- Federal or state income tax preparation, deductions, or estimated tax payments

- Sales tax registration, collection, and filing — covered in the multi-state sales tax operating guide

- Audit defense or response to an IRS or state DOR audit letter

- Reconciliation of payment processors other than Shopify Payments (the pattern is similar but the specific reports and field names differ)

- International sellers, non-resident sellers, or sellers not subject to US tax reporting

- Inventory accounting, cost of goods sold, or capitalisation

- Bookkeeping software setup or chart of accounts design

Operators who need help in any of the above categories should reach out to a qualified US tax professional, a CPA, an enrolled agent, or an attorney licensed in the relevant jurisdiction.

Practical next steps

What to do this week, in order:

- Locate the most recent 1099-K in Shopify admin → Settings → Payments → Shopify Payments → Documents. Save a dated PDF copy.

- Pull the seven Shopify reports listed in the “Shopify Payments records to export” section above for the same calendar year. Save them as a single dated CSV bundle.

- Run the 5-line-item model in a spreadsheet. The numbers will be illustrative until the actual exports are loaded; the goal is to confirm the structure works for the store.

- Cross-check the result against the Shopify “Total sales” report and against bank deposit totals. Confirm the residual gap is within roughly 1–2% of total sales.

- Investigate any larger gap using the “Common mismatch scenarios” section above. If the gap remains material, consider bringing in a CPA.

- Set up a monthly habit using the monthly reconciliation checklist. Treat it as a 15-minute monthly task rather than a 6-hour January project.

- Confirm Shopify Payments has the correct legal entity name and TIN on file, especially if any reporting threshold may be crossed this year, to avoid backup withholding.

The free 1099-K Reconciliation Sheet automates the five line items, accepts Shopify Reports figures, includes a Shopify Admin path map for each input, and outputs a status flag (OK / WATCH / REVIEW) based on the variance against your tax return. The sheet is the planned-asset companion to this article and was released alongside it.

For the broader registration and deregistration workflow, see Multi-State Sales Tax for Solo Shopify Stores: A 2026 Operating Guide.

1099-K Reconciliation Calculator

A reconciliation aid, not tax advice. Confirm figures with your books and a CPA.

Forvendo newsletter

Operating notes, once a week

One email a week for US-based solo Shopify operators at $5,000–$50,000 MRR: a decision, a checklist, or a teardown. No fluff, unsubscribe anytime.

Join the newsletter →Frequently Asked Questions

Do I need to send the reconciliation worksheet to the IRS with my return?

Generally no. The worksheet is internal documentation. It is shown if the IRS or a CPA asks for it during preparation or in response to a notice. Confirm with the IRS publication current at filing and a qualified preparer.

My 1099-K Box 1a includes amounts processed by a third-party gateway like PayPal or Shop Pay Installments. Are those double-counted?

Each payment settlement entity generally issues its own 1099-K. Shopify Payments issues for Shopify Payments transactions; PayPal issues for PayPal transactions; Affirm issues for Affirm transactions. The total payments processed across all platforms is the sum, not the largest single 1099-K.

What if I changed payment processors mid-year?

A 1099-K may be issued by each processor for the portion of the year that processor was active, provided each crossed its own reporting threshold. Each one should be reconciled separately, then summed.

Can I deduct Shopify Payments fees as an expense on Schedule C?

Processing fees are usually deductible as a business expense. Subtracting them from the 1099-K reconciliation and deducting them on Schedule C reflects the same dollars on two different forms, which is generally the correct treatment. Specific line placement should be confirmed with a CPA.

My state 1099-K threshold is $600. Do I still need to file a state return if my actual revenue was small?

When a state issues a 1099-K, the state generally expects a corresponding return. The return may show very low or zero tax owed, but a filing is usually expected. Confirm the current state filing requirement with the state Department of Revenue or a CPA familiar with that state.

What is the difference between gross payments and net business revenue?

Gross payments is the total dollar value of card and third-party-network payments processed before deductions, as reported on Form 1099-K Box 1a. Net business revenue is the figure reported on Schedule C (or the corresponding line on Form 1120, 1120-S, or 1065) after refunds, fees, chargebacks, shipping treatment, and sales tax collected are excluded. The two are related but measure different things.

What should I review monthly?

Shopify Payments exports for the month (transactions, payouts, refunds, fees), comparison of payout totals to bank deposits, and notes on chargebacks or unusual adjustments. A short monthly habit removes most of the January reconciliation burden.

When should a solo Shopify operator talk to a CPA?

When the reconciliation gap remains material after the five line items are subtracted, when an IRS or state DOR notice arrives, when backup withholding has been applied, when a mid-year processor or entity change happened, or when prior filings do not match. Reconciliation expertise across multi-processor ecommerce stores is a specific skill; ask about the CPA’s experience before engaging.

Can Shopify file my taxes for me?

No. Shopify Payments can issue Form 1099-K and provide reports. Filing tax returns is the seller’s responsibility (or the seller’s CPA’s responsibility). Calculation, reporting, and filing are separate activities.

Did OBBBA also change the 1099-NEC threshold for contractors I pay?

Yes. OBBBA raised the 1099-MISC and 1099-NEC reporting thresholds from $600 to $2,000, effective for tax year 2026 and adjusted for inflation starting in 2027. For a solo Shopify operator paying a virtual assistant, freelance designer, or other contractor, a contractor paid between $600 and $2,000 in 2026 no longer triggers a federal 1099-NEC requirement. State-level requirements may still apply — New Jersey, for example, retains a $1,000 1099 filing threshold that now sits below the federal $2,000. Confirm against each state’s information-return rules before deciding not to issue a 1099.

-

IRS, “Backup withholding.” Accessed 2026-05-20: https://www.irs.gov/businesses/small-businesses-self-employed/backup-withholding ↩

Forvendo Editorial note. Forvendo publishes educational operating resources for solo ecommerce operators. Articles may cover tax, sales tax, 1099-K reporting, software pricing, platform policies, and other operating topics that change over time.

This content is for general research and operational planning. It is not legal, tax, accounting, financial, or professional advice. Readers should verify details with official sources or qualified professionals before acting on them. Platform rules, tax thresholds, software pricing, and affiliate program terms can change without notice.

Forvendo articles may be drafted with AI assistance and are reviewed by the operator before publication according to our Editorial Policy, which covers sourcing, AI use, update cadence, and corrections. See also About, Disclosure, and Privacy Policy.